In June 2025, I posted an article analyzing more than a dozen Initiatives written by conservatives that had gathered hundreds of thousands of signatures, and won at the polls, only to be overturned by the Washington Supreme Court due to their failure to comply with various sections of the Washington State Constitution. In fact, over the past 24 years, there has only been one Conservative Initiative that survived a legal challenge (the Parents Rights Initiative in January 2025). On April 30, 2026, I posted a second article explaining why the 2026 Parents Rights and Girls Rights Initiatives also violated Article II, Section 37 of the Washington State Constitution – and will therefore be overturned should either of these Initiatives by passed by the voters in Fall 2026. In this article, we will once again review the Washington State Constitution requirements for drafting Initiatives and explain why the 2026 Income Tax Initiative will be overturned by the Washington Supreme Court should it be passed by the voters in Fall 2026. We will also explain why the best way to insure that an Income Tax Initiative complies with our State Constitution is to repeal the entire 2026 Income Tax law changes and not merely some of those law changes.

Three basic requirements for an Initiative to comply with the Washington State Constitution in order to survive a legal challenge

The 3 sections of our state constitution that need to be complied with are:

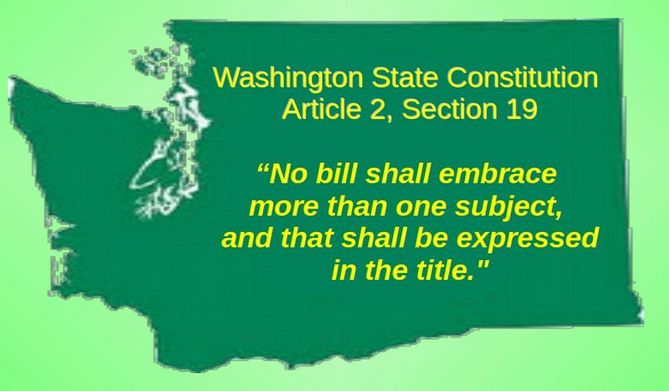

Article 2, Section 19, called the Single Subject Rule: “No bill shall embrace more than one subject, and that shall be expressed in the title.”

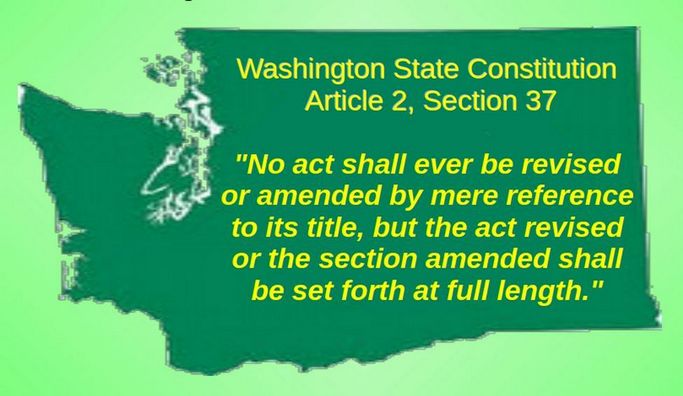

Article 2, Section 37 called the Full Text rule: "No act shall ever be revised or amended by mere reference to its title, but the act revised or the section amended shall be set forth at full length."

This means that the full text of the law or section of law being revised by the Initiative must be included in the Initiative submitted to the Secretary of State and must be printed in full on the back of every petition. Failing to include the full text can lead to the initiative being overturned.

Article 2, Section 22 of the Washington State Constitution also known as the Simple Majority Rule states in part: “a majority of the members elected to each house be recorded thereon as voting in its favor.”

An initiative must comply with all three of the above provisions. Violating even one provision renders the entire initiative to be void. In addition, an Initiative can not silently amend or ignore any Constitutional provision.

Summary of the 2026 Millionaires Income Tax Senate Bill 6346

Here is a link to the actual 109 page Senate Bill 6346 as passed by the Washington State legislature on March 11, 2026.

https://lawfilesext.leg.wa.gov/biennium/2025-26/Pdf/Bills/Senate%20Passed%20Legislature/6346-S.PL.pdf?q=20260515055649

Here is the summary of Senate Bill 6346 at the top of the first page:

“AN ACT Relating to investing in Washington families and businesses to fund K-12 education, health care, higher education, other essential governmental services, and the working families' tax credit, and to reduce certain sales and use taxes and certain business and occupation taxes by establishing a tax on millionaires; amending RCW 82.32.050, 82.32.060, 82.32.090, 2.10.180, 2.12.090, 2.14.100, 6.15.020, 41.24.240, 41.32.052, 41.34.080, 41.35.100, 41.37.090, 41.40.052, 41.44.240, 41.26.053, 41.28.200, 43.43.310, 82.08.0206, 82.04.4451, 82.32.045, 82.04.288, 82.04.050, 82.04.192, 82.04.050, 82.04.288, and 1.90.100; amending 2023 c 456 s 3 (uncodified); adding a new section to chapter 74.20A RCW; adding new sections to chapter 82.08 RCW; adding new sections to chapter 82.12 RCW; adding a new Title to the Revised Code of Washington to be codified as Title 82A RCW; creating new sections; prescribing penalties; and providing effective dates.”

In plain English, Senate Bill 6346 amends 27 existing laws, adds new sections to 3 existing laws and adds a new Title 82A to the Revised Code of Washington (RCW).

Existing laws are amended by striking out words that would no longer apply and underlying words that are added to the law. To make these 31 changes, the 109 pages of Senate Bill 6346 are divided into the following 12 Parts:

Part 1 Definitions

Part 2 Determination of Tax

Part 3 Adjusted Gross Income Modifications

Part 4 Division of Income

Part 5 Estimated Tax Payments

Part 6 Crimes

Part 7 Administrative Provisions

Part 8 Application of Tax to Public Pensions

Part 9 Tax Relief

Part 10 Definitions of Retail Sales

Part 11 Clarifying Definitions of Retail Sales

Part 12 Miscellaneous

These 12 Parts are further divided into 93 sections. Each of these 93 Sections has its own title.

Note that Parts 1 through 8 define the process for calculating the State Income tax – which is estimated to generate about $4 billion a year in annual revenue. Part 9 uses about $2 billion of the $4 billion to provide tax relief for certain low income families and certain small business owners as well as about $320 million in childcare subsidies.

All bills drafted by the legislature are reviewed by the Code Revisers office to insure they are in harmony with existing laws

It is important to note that Senate Bill 6346 was reviewed by the Washington State Code Revisers office. The Code Reviser is a State of Washington government official responsible for harmonizing the laws of the state and advising legislators on the preparation of bills.

This office was created by the Washington State legislature in 1950 and is also responsible for publishing the Revised Code of Washington (RCW). The revised code of Washington is used by judges to determine and enforce Washington State laws. The Code Reviser’s office also publishes an 87 page Bill Drafting Guide which was revised in 2025 and explains how to draft bills that comply with our State Constitution and can be harmonized with existing Washington State laws. The Code Reviser employs a professional staff of about 40 people.

On page 12 of the Bill Drafting Guide, the Code Reviser shows how to write a bill or initiative that repeals more than one section of existing state laws:

Repealing more than one section of the RCW. Use subsection groupings, cite each RCW section to be repealed, the section caption, and its session law history, from most current to original. For example:

NEW SECTION. Sec. 1. The following acts or parts of acts are each repealed:

(1) RCW 70A.210.040 (Actions by municipalities validated) and 1975 c 6 s 4;

(2) RCW 70A.210.050 (Municipalities—Revenue bonds for pollution control facilities—Authorized—Construction— Sale, conditions—Form, terms) and 1983 c 167 s 174, 1975 c 6 s 3, & 1973 c 132 s 5;

(3) RCW 70A.210.060 (Proceeds of bonds are separate trust funds—Municipal treasurer, compensation) and 1975 c 6 s 2; and

(4) 2002 c 301 s 1 (uncodified)

Note that only the titles of the laws or parts of laws being repealed need to be included. Sadly, the Income Tax Initiative fails to include any of the titles of laws being repealed. On page 40 of the Bill Drafting Guide, the Code Reviser states:

Amending without setting forth in full—Amendments to sections by reference.

(i) Article II, section 37 of the state Constitution provides, "No act shall ever be revised or amended by mere reference to its title, but the act revised or the section amended shall be set forth at full length."

The purpose of this constitutional provision is to inform the legislature and the public as to the nature and effect of proposed and enacted statutes. It is not intended to restrict or hamper the legislature, but to regulate the method of enactment.

(ii) This is an example of amending a section by mere reference:

NEW SECTION. Sec. 1. A new section is added to chapter

43.21A RCW to read as follows:

Notwithstanding the provisions of RCW 15.54.480, fertilizer inspection fees must be deposited into the water quality account.

Generally, this requirement does not apply to supplemental acts that do not modify or alter the original act in any way, to acts that merely add new sections to an existing act, or to acts complete in themselves, not purporting to be amendatory, but that by implication amend other legislation on the same subject. On the other hand, the courts are equally emphatic that if an act is not complete in itself and is clearly amendatory of a former statute, it falls within the constitutional inhibition whether it purports on its face to be amendatory or an independent act…

In Washington Education Assoc. v. State 93 Wn.2d 37, 40-41 (1980), the court expressed the issue with two questions:

(A) Is the new enactment such a complete act that the scope of the rights or duties created or affected by the legislative action can be determined without referring to any other statute or enactment?

(B) Would a straight-forward determination of the scope of rights or duties under the existing statutes be rendered erroneous by the new enactment?

How to read a particular law in the Revised Code of Washington

The RCW is a three-tier structure: Titles, Chapters, and Sections:

Title — The broadest grouping of subjects. The current RCW contains 91 active titles. Title 82 covers Excise Taxes and Title 84 covers Property Taxes. Senate Bill 6346 created a new Title called 82A.

Chapter — Each title is subdivided into chapters addressing a specific subtopic. Title 82 contains more than 60 chapters such as retail sales tax (RCW 82.08) and capital gains tax (RCW 82.87).

Section — A section contains the operative text of a single statutory provision. Sections are cited in the format RCW [Title].[Chapter].[Section] — for example, RCW 82.87.020 identifies Title 82, Chapter 87, Section 020, which defines capital gains.

An example of an Initiative with a properly stated repeal section

In 2016, Initiative 1464 was a 23 page Initiative that included a section repealing two laws. Here is the summary:

AN ACT Relating to accountability of Washington's system of electoral politics to the people; amending RCW 42.17A.400, 42.17A.430, 42.17A.445, 42.17A.645, 42.17A.470, 42.17A.050, 42.17A.750, 42.17A.755, 42.17A.765, and 42.17A.125; adding new sections to chapter 42.17A RCW; adding a new section to chapter 82.32 RCW; creating new sections; repealing RCW 82.08.0273 and 42.17A.550; prescribing penalties; and making appropriations.

On Page 22, the repeal section, the Initiative stated:

NEW SECTION. Sec. 30. The following acts or parts of acts are each repealed:

(1) RCW 82.08.0273 (Exemptions—Sales to nonresidents of tangible personal property, digital goods, and digital codes for use outside the state—Proof of nonresident status—Penalties) and 2014 c 140 s 17, 2011 c 7 s 1, 2010 c 106 s 215, 2009 c 535 s 512, 2007 c 135 s 2, 2003 c 53 s 399, 1993 c 444 s 1, 1988 c 96 s 1, 1982 1st ex.s. c 5 s 1, & 1980 c 37 s 39; and

(2) RCW 42.17A.550 (Use of public funds for political purposes) and 2008 c 29 s 1 & 1993 c 2 s 24.

Note that in keeping with the advice from the Code Revisers Bill Drafting Guide, only the titles of the laws or sections of laws being repealed were included. Still, these brief descriptions can alert a voter about the topic of the law or section of law which the voter can then further research if the voter is interested in that topic.

Problems with Initiative 26-645 – The Income Tax Initiative

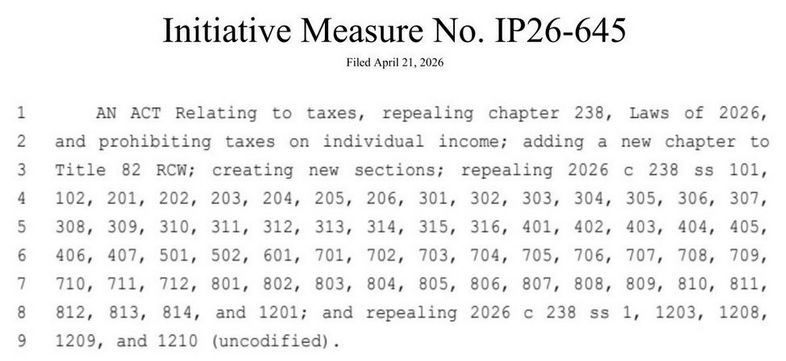

Initiative 26-645 which can be downloaded from this page by scrolling to the bottom of the page and clicking on IP26-645, View Complete Text.

Here is the Ballot Title of the Initiative:

Initiative Measure No. IP26-645 concerns state and local taxes.

This measure would repeal a 9.9% tax on annual individual income over $1,000,000; prohibit taxes measured by individual income and taxes on individual income or the receipt of individual income; and define “income.”

Here is the Ballot Measure Summary: “This measure would repeal a 9.9% tax on annual individual income over $1,000,000; prohibit state and local governments from imposing taxes on individual income or the receipt of individual income and taxes measured by an individual’s income; and define income as “any gain or benefit measured in money derived from an individual’s capital, labor, property, or other source.” It would also define “individual” as a natural person for purposes of excise taxes.“

In contrast with the 109 page Income Tax bill, the Income Tax Initiative is only 4 pages long. Here is the summary of the Initiative on the first page:

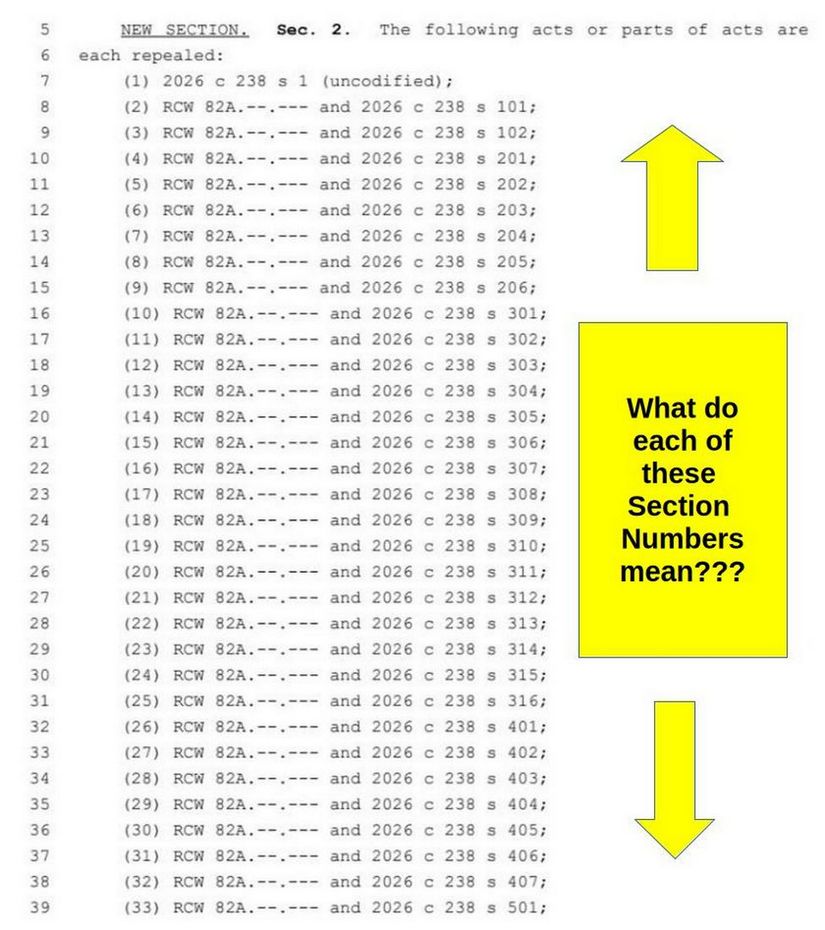

On page 2 is another summary of the parts of the Act which are repealed:

Note that there is no explanation of what each section being repealed states. Here is an alternative that would have at least given voters a clue as to what was in each section by including at least the titles of each section:

Sec. 1. INTENT

Sec. 101. DEFINITIONS.

Sec. 102. UNDEFINED TERMS—CONFORMITY WITH FEDERAL INTERNAL REVENUE CODE

Sec. 201. TAX IMPOSED—RATES.

Sec. 202. DISTRIBUTION OF TAX REVENUES.

Sec. 203. CREDIT FOR INCOME TAXES DUE TO ANOTHER JURISDICTION.

Sec. 204. CREDIT FOR BUSINESS AND OCCUPATION AND PUBLIC UTILITY TAXES.

Sec. 205. CREDIT FOR WASHINGTON CAPITAL GAINS TAXES.

Sec. 206. CREDIT FOR PASS-THROUGH ENTITY TAX PAYMENTS.

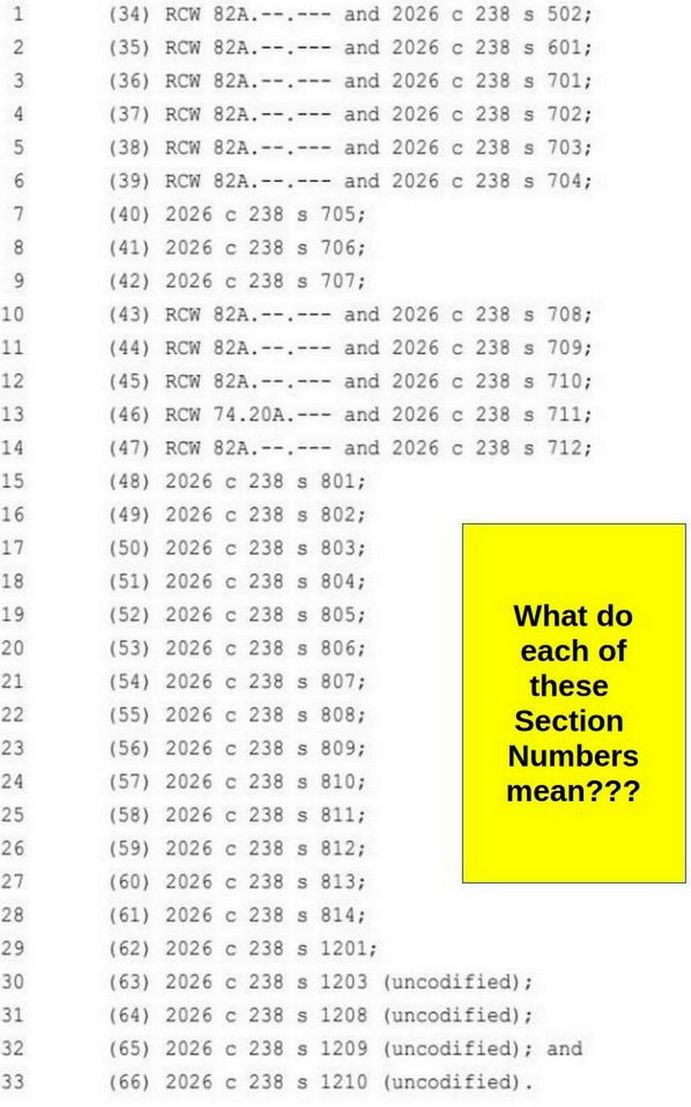

Here is a screen shot of the remaining sections being repealed on page 3:

The problem with pages 1, 2 and 3 of the Initiative is that the voters have no idea of the actual text in all of these sections that are being repealed.

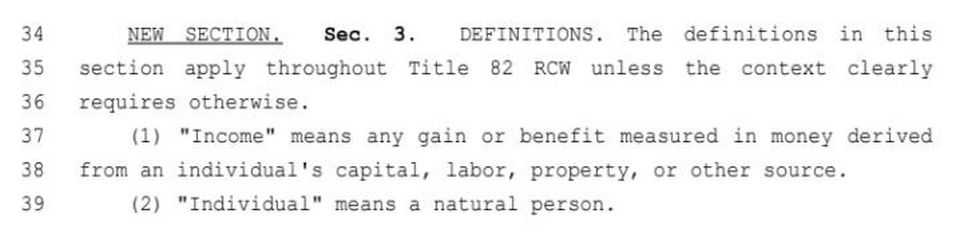

At the bottom of page 3 is a new section called DEFINITIONS:

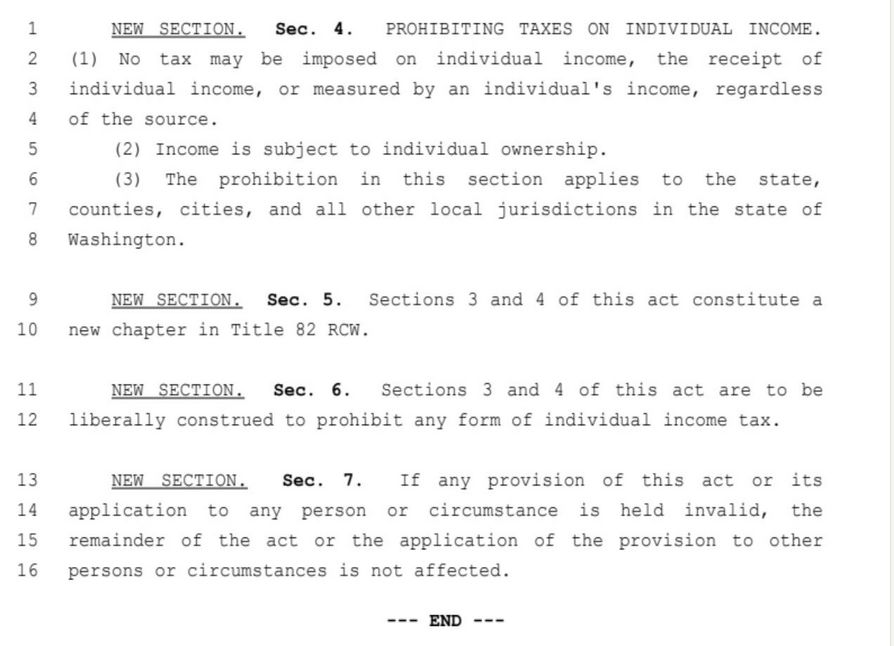

Finally, here is a screen shot of page 4 which includes four new sections.

In summary, if Initiative 645 is passed by the voters and certified by the Washington Supreme Court as complying with our State Constitution, it would repeal all sections of Senate Bill 6346 from Section 101 to Section 814 but would leave in place Sections 901, 902, 903, 904, 905, 906, 907, 908, 909, 910, 911, 912, 1001, 1002, 1003, 1101. 1102, 1103, 1104, 1105, 1106, 1107. Then it would repeal Sections 1201, 1203, 1208, 1209 and 1210 while leaving in place Sections 1202, 1204, 1205, 1206 and 1207.

Again, the problem with failure to include the actual text of all of these sections - or at least the titles of these sections - is that voters have no idea of what is actually being repealed from the Income Tax bill versus what is in the sections being retained. It is only by carefully reading each of the above sections in the original bill and comparing each section to the Initiative that a voter might learn that the Initiative would repeal the $4 billion per year in Income Tax provisions in Part 2 but retain the $2 billion per year in Tax relief provisions in Parts 9, 10 and 11. The tax relief provisions are the extension of the Working Families Tax Credit, the expansion of the Small Business Tax Exemption and the increase in Child Care subsidies.

However, Section 1 Intent Item #11, at the bottom of Page 3 and top of Page 4 states in part: “The legislature further intends that the tax imposed under this act operate together with certain tax reductions and tax credits enacted by this act as an integrated reform of the state tax code, and that repeal or invalidation of section 201 of this act would reinstate certain sales and use tax on items made exempt by this act and repeal working families tax credits and small business tax credits enacted by this act.”

The Initiative repeals Section 1 and repeals the Income Tax in section 201 - but does not repeal the billions of dollars in Tax Relief offered in Section 9 10 and 11. If the Initiative were approved, it would either lead to a $2 billion hole in the state budget – or the repeal of the $2 billion in Tax Relief supposedly retained in the Initiative.

In addition, the Initiative appears to silently repeal the Capital Gains tax. Look carefully at the Definition of Income in the New Section 3 on page 3 of the Initiative:

“Income” means any gain or benefit measured in money derived from an individual’s capital, labor, property or other source.”

Thus, the Income Tax Initiative is clearly in violation of Article 2, Section 37 of our State Constitution which states: "No act shall ever be revised or amended by mere reference to its title, but the act revised or the section amended shall be set forth at full length."

This means that the full text of the law or section of law being revised or amended by the Initiative must be included in the Initiative submitted to the Secretary of State and must be printed in full on the back of every petition. Failing to include the full text of the law or section of law being revised will lead to the initiative being overturned.

The Income Tax Initiative does the opposite of what is required. Instead of including the full text, it merely indicates the Section numbers being repealed – and says nothing about the Section numbers in Senate Bill 5346 which are not being repealed. Voters are left in the dark about what will happen to billions of dollars in new tax credits created by Senate Bill 5346. The Initiative also hides the fact that it is repealing the capital gains tax.

Washington Supreme Court rulings on Article 2, Section 37 of the Washington State Constitution

In 1975, the legislature passed a bill which silently amended an existing state law by being slipped into a 45-page appropriations bill only by reference to the law being amended without including the actual text of the law being amended. In Flanders v. Morris, (1977), this type of silent amendment was ruled to violate Article 2, Section 37 of the Washington state constitution. Here are quotes from this ruling:

“The reason for requiring amendatory legislation to set out the statute in full was stated in the 1959 Washington Toll Bridge Authority case, quoting from State ex rel. Gebhardt v. Superior Court, 15 Wn.2d 673, 685, 131 P.2d 943, 949 (1942):

"The section of our constitution above referred to was undoubtedly framed for the purpose of avoiding confusion, ambiguity, and uncertainty in the statutory law through the existence of separate and disconnected legislative provisions, original and amendatory, scattered through different volumes or different portions of the same volume. Such a provision, among other things, forbids amending a statute simply by striking out or inserting certain words, phrases, or clauses, a proceeding formerly common, through which laws became complicated and their real meaning often difficult of ascertainment. The result desired by such a provision is to have in a section as amended a complete section, so that no further search will be required to determine the provisions of such section as amended."

“Another important purpose of Const. art. 2, § 37, not mentioned above, is the necessity of insuring that legislators are aware of the nature and content of the law which is being amended and the effect of the amendment upon it. “

In 1982, the foundational framework for evaluating Article 2, Section 37 challenges was set in Washington Education Association v. State (1982). In this decision, the Washington Supreme Court established a two-part test to determine if legislation unconstitutionally amends an existing law without setting it forth at full length:

Part 1 question: Does the new legislative enactment or Initiative change the scope of rights or duties under an existing statute? In other words, does the Initiative amend existing laws or is it a “complete” and independent act which does not amend any existing laws? If the Initiative amends existing laws, then it must comply with Article 2, Section 37 and include the complete text of laws being amended.

Part 2 question: Can the straightforward determination of rights and duties under the prior enactment still be made without reference to the new law, or does the new law render the old law's straightforward determination erroneous?

If the enactment requires a reader to flip back and forth between multiple statutes to decipher what the law actually says and does, it violates Section 37.

First, the Income Tax Initiative amends existing laws and is not a complete or independent law. This Article 2, Section 37 applies. Second, by amending or repealing many sections in the existing income tax law while leaving many other sections in place, the Income Tax Initiative by failing to include the complete text, requires several hours of flip back and forth between multiple statutes to decipher what the law actually says and does.

In 2007, in a case called Washington Citizens Action of Washington v. State, the Washington Supreme Court struck down Initiative 747, which limited annual property tax levy increases to 1%, for violating Article 2, Section 37. The court ruled that the initiative’s text claimed to reduce the property tax levy limit from 2% to 1%, but it actually amended existing laws that set the cap at 6%, thus failing to disclose the true impact and accurately set forth the law being amended.

Here are quotes from this ruling:

“Article II, section 37 is intended both to ensure disclosure of the general effect of the new legislation and to show its specific impact on existing laws in order to avoid fraud or deception.”

“Citizens or legislators must not be required to search out amended statutes to know the law on the subject treated in a new statute. Under article II, section 37, a new statute must explicitly show how it relates to statutes it amends… Thus, a significant purpose of article II, section 37 is to ensure that those enacting an amendatory law are fully aware of the proposed law's impact on existing law.”

“Washington Constitution article II, section 37 requires the legislature to set forth the full length of the relevant act or section to be amended… The text of the initiative misled voters about the substantive impact of the initiative on existing law… The purpose of article II, section 37 is to avoid misleading voters or legislators as to the effect an initiative will have on existing law. “

“Article II, section 37 was designed to protect voters and legislators from confusing or misleading information and to maintain the integrity of the law-making process… We have typically analyzed, as an initial matter, whether the legislation at issue is amendatory of prior acts or complete in and of itself, thereby making the new legislation exempt from the article II, section 37 requirement. “

“First, the court must determine whether the bill is such a complete act that the scope of the rights created or affected by the bill can be ascertained without referring to any other statute or enactment. Second, would a determination of the scope of the rights under the existing statutes be made erroneous by the bill?”

“The purpose of the second prong is to ensure that those impacted by a particular existing law can evaluate the impact of the proposed amendment on that existing law.”

“Nothing about the test speaks to whether a clearly amendatory act such as this one has adequately or correctly set forth the law that it seeks to amend. Applying the above test, we conclude that the parties were correct to conclude I-747 is amendatory in character and thus article II, section 37 is applicable… The purpose of article II, section 37 is to avoid misleading those voting on a proposed law by ensuring disclosure of the general effect of the new legislation by showing its specific impact on existing laws. Because article II, section 37 is intended to protect those who are to vote on amendatory legislation from fraud and deception, we consider compliance with the provision at the time of the operative vote. “

The only exception to Article 2 Section 37 are “complete” acts. Here is an example of the “complete act” exception:

In 2000, voters passed Initiative 713 which banned certain kinds of traps for catching wildlife. This Initiative was challenged by a group which claimed that it violated Article 2, Section 37. In 2003, the Supreme Court issued a decision in Citizens for Responsible Wildlife Mgmt v State (2003) concluding that Initiative 713 complied with Article 2, Section 37.

Here are quotes from this ruling:

“The purpose of section 37 is to "protect the members of the legislature and the public against fraud and deception; not to trammel or hamper the legislature in the enactment of laws." Spokane Grain & Fuel Co. v. Lyttaker, 59 Wash. 76, 82, 109 P. 316 (1910). An act is exempt from section 37 requirements if the act is complete, independent of prior acts, and stands alone on the particular subject of which it treats.”

“Is I-713 Amendatory of Prior Acts or Complete? An act is amendatory in character, rather than complete, if it changes the scope or effect of a prior statute, and therefore must comply with section 37.”

“First, the court must determine whether the bill is such a complete act that the scope of the rights created or affected by the bill can be ascertained without referring to any other statute or enactment. Id. Second, would a determination of the scope of the rights under the existing statutes be made erroneous by the bill?”

“Citizens contend that I-713 is not a complete act because the effect of the initiative is not readily ascertainable as it alters the rights of landowners, conferred by RCW 77.36.030, to trap or kill wildlife causing damage without reference to that statute. This, Citizens urge, is directly contrary to the purpose behind section 37 which is to "avoid confusion, ambiguity and uncertainty in the statutory law through the existence of separate and disconnected legislative provisions, original and amendatory, scattered through different volumes or different provisions of the same volume."

“Under the first prong of the test, the effect of I-713 is readily ascertainable from the words of the statute alone. By its own terms, I-713 clearly bans the use of body-gripping traps to trap any animal for recreation or commerce in fur, or for any other purpose without engaging the special permit process provided… The first prong of the test is satisfied, i.e., the scope of the rights created or affected by I-713 can be ascertained without referring to any other statute or enactment.”

“As to the second prong, Citizens vie for a strict interpretation of section 37 and its requirements, contending that I-713 fails because it does not set forth statutes that it amends… They argue that I-713 creates ambiguity as to RCW 77.36.030, leaving a landowner who reads RCW 77.36.030 unaware of what his rights are regarding trapping problem animals.”

“(But) I-713 does not change a landowner's right to trap; it regulates the types of traps that may be used. In this way, the initiative does not alter preexisting rights or duties to an impermissible degree.”

What would a Constitutionally valid Income Tax repeal Initiative look like?

The secret to a valid repeal Initiative is to repeal the entire act, namely to repeal all of Senate Bill 5346 – with no additions or subtractions. If done this way, there would be no silent amendments to worry about and no budget conflicts to overcome. As with a Referendum, voters would easily understand that the law was being returned to the law that existed prior to the enactment of the bill. This simple approach has the further benefit of reducing the risk of the Initiative being in violation of Article 2, Section 19 (the Single Subject rule) as the legislature has a huge staff of attorneys in the Code Revisers office to help warn them if a bill needs to be split into two bills to comply with this Constitutional provision.

What will be the end result for this fatally flawed Income Tax Initiative?

The Income Tax bill is so widely opposed that it should have no trouble getting the 400,000 signatures in the next 40 days. It is likely that volunteers will be able to collect at least 100,000 signatures and $3 million from a few wealthy people will supply the other 300,000 signatures needed by using paid signature gatherers.

If it makes it to the Fall 2026 ballot, the Income Tax repeal Initiative is likely to be approved by the voters by a wide margin. Within a week of passing the voters, the Initiative will be challenged by some group that will certainly refer to Article 2, Section 37 of the Washington state constitution. They will point out that the Income Tax Initiative did not even include the Titles of the Sections that were repealed. It was just a bunch of Section numbers.

As with the Natural Gas Initiative, a King County judge will rule that the Initiative was unconstitutional. The BIAW and or Lets Go Washington will appeal to the Washington Supreme Court – which will affirm the lower court ruling in a years long process that only benefits a couple of attorneys.

But in addition to the Income Tax Initiative, two other poorly written Initiatives will be on the ballot and likely passed by the voters. Both of these Initiatives also violate Article 2, Section 37 as both silently amend and conflict with existing state laws as I have explained in this article.

These two Initiatives will also be challenged and rejected by our Supreme Court. To add insult to injury, in the next few months, there will be a ruling on the Natural Gas Initiative – which will also be held to violate Article 2, Section 37. Thus by the beginning of the 2028 statewide and national election, conservatives will have lost four major Initiatives simply due to a failure to respect Article 2, Section 37 of the Washington state constitution.

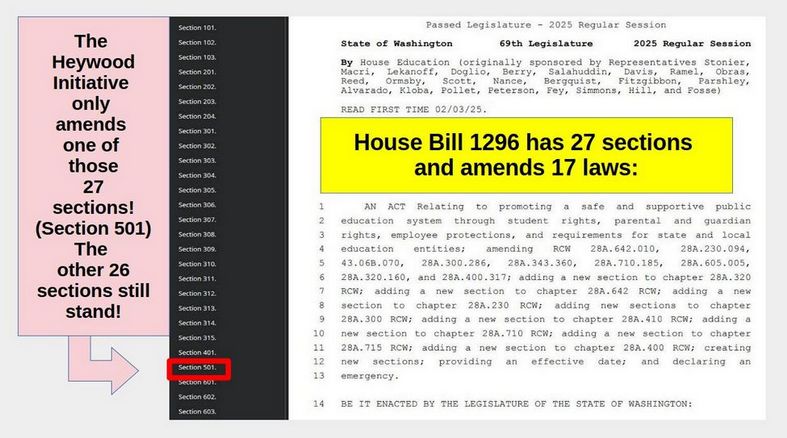

Consequences of a series of poorly written Initiatives

Over the past 26 years, conservative volunteers have spent tens of thousands of hours and invested tens of millions of dollars in trying to pass more than 20 conservative Initiatives. Only one of these Initiatives was able to withstand a legal challenge (the Parents Rights Initiative in 2024). But even this Initiative was voided in 2025 by House Bill 1296. Imagine what would happen if a baseball team or a football team went zero for twenty? At a bare minimum, they would be looking for a new manager.

But also imagine what would have happened if conservatives did a better job of writing Initiatives. I few real Initiative victories might result in better policies taking effect in our state – and less out of control tax and spend policies. At the very least, some real victories would cause the crazies who run Olympia to think twice before passing radical laws.

But imagine of all of the volunteer hours and millions of dollars spent getting signatures were instead spent on electing conservative candidates to the legislature – or electing a more conservative governor. Instead, what we have seen for the past 26 years is the longest and worst losing streak in Washington State political history.

My mom used to say: “Fool me once, shame on you. Fool me twice, shame on me. “

How many times do we need to be fooled by badly written Initiatives before we demand changes to this entire process? Here are two specific proposals that can be used by any county political organization to help avoid another repeat of the Income Tax Initiative fiasco.

Better Process for writing Initiative… An Initiative drafting committee

Right now, the Washington State Republican Party has an Election Integrity Committee that meets every month – and they are doing great work on improving the accuracy of our elections here in Washington state. It would be an easy matter to form an Initiative Drafting committee and recruit volunteers willing to learn about recent Washington Supreme Court rulings on badly written Initiatives.

This committee could review potential Initiatives to insure that they comply with Article 2, Section 19 and Article 2, Section 37 – and make the changes needed to make sure that conservative Initiatives complied with our State Constitution before being sent to the various county organizations.

This would be dramatically better than the current unreliable system where a single person writes the Initiative and submits it to the Secretary of State – typically without any public review of the Initiative before it is submitted to the Secretary of State. Initiatives like laws should go though at least some kind of committee review and improvement process.

Better Process for endorsing Initiatives… An Initiative Endorsement committee

Most county political organizations have committees for endorsing candidates. But they apparently endorse Initiatives without even the slightest of concerns as to whether they comply with the Washington State Constitution. Instead of rubber stamping what ever state leaders put out, it would be better for accountability for each county to have its own Initiative Endorsement Committee which can make independent recommendations after hearing from both supporters and opponents of any given Initiative.

Addressing the Real Problem… Out of Control State Spending

“We do not have an income problem. We have a spending problem.”

Chris Gregoire, Former Washington Governor, May 6, 2026

The real problem with the Income Tax Initiative is that it will not only suck another $4 billion out of our economy, it will also give our insane legislature another $4 billion in tax dollars to further expand our extremely bloated and extremely corrupt state government.

The Washington State budget has skyrocketed in just the past 14 years from about $15 billion per year in 2012 to more than $45 billion in 2026. This tripling in the size of state government has been accompanied by a tripling in state taxes – and this is before the added $4 billion from the Income Tax – which does not even take effect until 2029.

By comparison, the population of Washington increased from 7 million in 2012 to 8 million today – a total increase of 14%. Total Inflation in Washington state since 2012 according to the BLS Consumer Price Index for all Items in Seattle as reported by the Federal Reserve Bank on May 25, 2026 was 58% (rising from an Index of 240 to 380). The total increase for both population and inflation was 72% - meaning that any rational budget would be about $20 billion a year – not $45 billion a year.

The real solution to this out-of-control state spending is to dramatically reduce the size of our state government – for example, by cutting government spending in half or more… and to support real tax reform – for example by cutting the sales tax in half and by cutting property taxes in half. Even this reform would only return us to the huge state government we had back in 2012.

Three Constitutional proposals to cut state taxes in half and cut state government waste fraud and abuse in half

Instead of continuing to ignore the Washington State Constitution, conservative leaders should promote tax reform policies to comply with our State Constitution and help middle class families.

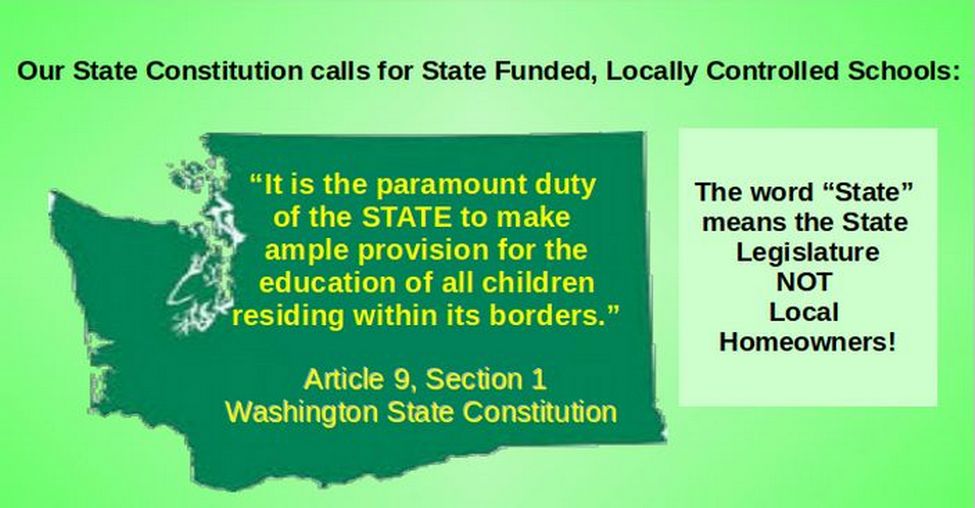

Constitutional proposal #1 An Initiative to honor Article 9, Sections 1 and 2 of our State Constitution

Article 9, Sections 1 and 2 of our State Constitution requires State funded and locally controlled public schools. Instead, our legislature has passed a series of unconstitutional laws over the past 10 years which have led to locally funded and state controlled public schools.

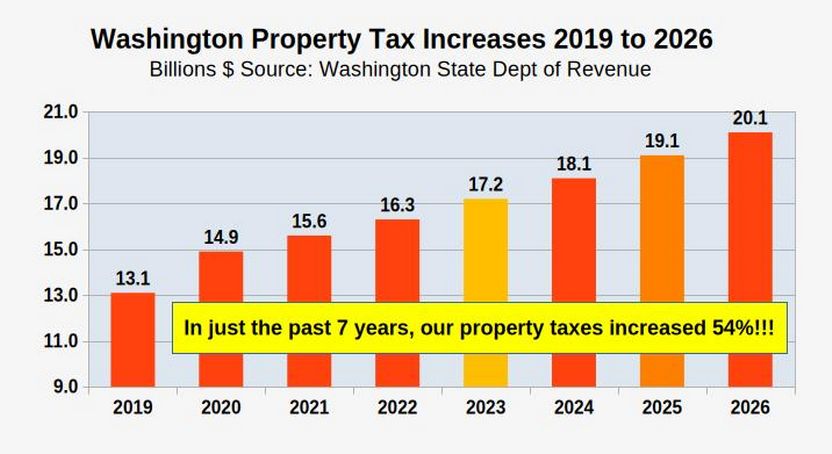

In the 1980’s, our Supreme Court ruled that local “enrichment” levies could not exceed 10% of state school funding. Yet since 2019, the local operating cost increased from 12% to 15% of school funding – costing local homeowners an additional billion dollars a year. But this is just the tip of the ice berg. In the 1980’s, the state paid for about 90% of school construction costs and local homeowners paid the other 10%. Today, that responsibility has been turned upside down with local homeowners being forced to cover 90% of school construction costs while the state only pays 10%. Combined, this transfer of the school funding burden has led to huge 54% increase in local property taxes in just the past 6 years.

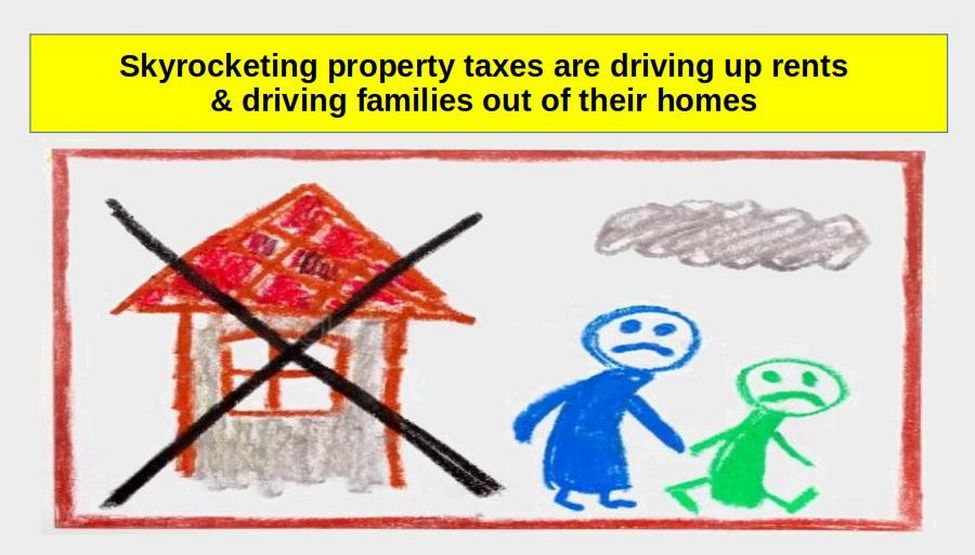

These huge property tax increases will drive up monthly rental costs and drive many families out of their homes. Washington state is already one of the least affordable states to live in the entire nation. Whether families rent or own their home, the last thing families need is a huge increase in state taxes. Families urgently need property tax relief that honors Article 9, Sections 1 and 2 of our State Constitution.

Constitutional proposal #2 An Initiative to honor Article 7, Section 10 of our State Constitution

We need an Initiative to restore the only property tax break allowed by our State Constitution – the Homestead Exemption for Retired Persons.

Article VII, Section 10 states: “The following tax exemption shall be allowed as to real property: The legislature shall have the power, by appropriate legislation, to grant to retired property owners relief from the property tax on the real property occupied as a residence by those owners.”

It is a fact that many retired persons are forced to sell their homes because they are living on a fixed income and can not afford the ever increasing property taxes. The median home value in Washington state is currently $600,000 and is increasing rapidly. This is 50% higher than the national average home value which is about $400,000. We should begin by exempting the first $400,000 of home value for any retired person who is over the age of 65 with the goal of eventually exempting the first $600,000 of home value for any retired person over the age of 65.

Reducing Property Taxes Helps Families with Children

The current property tax rate in Washington state is over one percent meaning that the average family faces a property tax bill of at least $6,000 per year or $500 per month. If we can roll this property tax bill back to under $3,000 per year (which is about what it was 20 years ago), we can save the average family $250 per month. This will not only allow families to put food on the table, but it will allow them to retain their family home and allow their children to remain in their local schools and retain their friendships with other local children. Many studies have shown that one of the best ways to maintain childhood mental health is by providing children with a stable home and community environment. Instead of driving families out of their homes with excessive property tax increases, we should be helping them stay in their homes by greatly reducing their property taxes.

Constitutional Proposal #3 An Initiative to lower child care costs

Anyone needing childcare in Washington state knows that the cost of childcare has skyrocketed during the past 9 years. The average cost of childcare providers in Seattle is now $1500 per month – or $18,000 per year. In East King County, the cost is over $2,000 per month or $24,000 per year. The average cost in the rest of our State is $1000 per month or $12,000 per year. The average family in Washington now pays 18% of their income on childcare. This is double what families used to pay for childcare here in Washington.

This huge increase in the cost of child care in the past 9 years was caused by a 264 page monster bill regulating child care called House Bill 1661 passed by our insane legislature in 2017.

This bill created the Department of Children, Youth, and Families (DCYF) or the Child Care Gestapo to oversee all state-licensed child care in our state. This bill essentially wiped out almost half of the local in-home child care providers – folks who were not able or willing to jump through all of the state regulation hoops.

It used to be that about half of all childcare (or about 100,000 slots) was provided by informal local In Home “mom and pop” Childcare providers – with the other half provided by large national chain corporations (another 100,000 slots).

In 2019, the Washington State Child Care Collaborative Task Force commissioned a survey of Washington parents. They found that Washington state had the third highest child care cost in the nation. They also found that the number of Child Care slots had declined by 20% by 2019 from about 220,000 to 180,000. This entire decline of 40,000 slots was due to small local In Home Childcare providers deciding that the massive regulations were simply not worth it. Put in plain English, while the national corporation childcare providers did not decline at all, there was a decline of 40% in the number of local In Home Childcare providers – from about 100,000 slots to about 60,000 slots.

As a consequence, half of all parents surveyed in 2019 stated they were unable to find any openings at any price near either their home or work. One in four said they could simply not afford child care. This has led to 135,000 parents either quitting their jobs or being fired – simply because of being unable to work because they could not find anyone to care for their child.

The cost to employers of parents either quitting their jobs or missing work was over $2 billion per year. This was in addition to the cost to parents of having their child care costs doubled. And it was in addition to the cost to tax payers of paying for the child care gestapo regulators.

The legislature’s “solution” to this problem has been to subsidize child care to the tune of hundreds of millions of dollars a year., But this just created a new problem called “ghost Childcare programs.” These are criminal outfits ripping off the tax payers to pay the child care for children who do not exist in day cares that do not exist.

Our Solution to the Childcare Crisis is to eliminate the regulations that caused this problem in the first place. This childcare crisis was created by the assumption that all parents and all childcare providers abuse children. This assumption is not correct. The vast majority of parents and In Home Childcare providers do not abuse their children. If a parent or childcare provider does abuse a child, they can and should be reported to Child Protective Services (CPS). There is simply no need for another massive State agency whose sole function is to drive up the price of childcare. Loving parents and devoted In Home Childcare providers should not have to be driven into poverty or out of business by a few bad apples. Our solution is to return to the Fifth Amendment of the US Constitution – that all parents and childcare providers are presumed to be innocent until proven guilty. Deregulating In Home Childcare providers will attract thousands of local In Home Childcare providers which will bring the cost of childcare back down to where it was 9 years ago – saving families thousands of dollars every year in child care costs and restoring local community jobs in the process.

Conclusion

If you agree that it is time for real tax reform, then join our Washington Parents Network and start attending our monthly meetings which are held on the first Sunday of every month from 4 to 5 pm. Our June 2026 meeting will be on June 7th. If you have any questions, or if you would like the link for our next meeting, email me – and please share this article with anyone you know who is interested in ending the war against our families.

Regards, David Spring M. Ed.