Last week, I wrote a 25 page article explaining why the Washington Supreme Court was likely to rule that the 2026 Income Tax Initiative violated Article 2, Section 37 of the Washington State Constitution. I got a huge number of emails with questions about the article. Therefore, I decided that this second article is needed in order to clarify why I believe that the Income Tax Initiative, as currently written, is fatally flawed and is almost certain to be overturned by the Washington Supreme Court.

Before getting into these concerns, I want to make a couple of points clear. First, while I am not an attorney, I have spend more than 20 years researching the Washington State Constitution and reading Washington Supreme Court opinions related to our State Constitution. Any of us can and should read the Washington State Constitution. You do not need to be an attorney to read and understand our State Constitution. If you are going to write or support an Initiative, you should read

n order to better understand the meaning of Article 2, Section 37, I read all of the Supreme Court decisions on Article 2, Section 37 going back 60 years. I quoted several of these Court decisions in my prior article. For example, in Flanders v. Morris, (1977), the Supreme Court stated: “Another important purpose of Const. Art. 2, § 37... is the necessity of insuring that legislators are aware of the nature and content of the law which is being amended and the effect of the amendment upon it. “

In 2007, in a case called Washington Citizens Action of Washington v. State, the Washington Supreme Court struck down Initiative 747 stating: “Article II, section 37 is intended both to ensure disclosure of the general effect of the new legislation and to show its specific impact on existing laws in order to avoid fraud or deception… Article II, section 37 was designed to protect voters and legislators from confusing or misleading information and to maintain the integrity of the law-making process.”

In short, the Initiative must provide enough information for voters to know what they are actually voting on. Thus, deleted sections of law must at the very least include the section captions of the deleted sections.

Second, tens of thousands of volunteer hours and millions of dollars in donations are currently being spent getting the Income Tax Initiative on the ballot. Even more thousands of hours and millions of dollars will be spent getting the Initiative passed by the voters this fall. It is certain that the Income Tax Initiative will be challenged should it be passed by the voters and it will be up to the Supreme Court to decide whether it violates Article 2, Section 37. Imagine the disappointment of all these volunteers if, after investing all of their time and money, the Income Tax Initiative is overturned by the Supreme Court simply because it was poorly written.

Third, in writing the article, it was not my intention to make “personal attacks” against the drafters of the Initiative. Nor was it my intention to “help the Democratic Party.” Instead, as I explained in my previous article, I am trying to prevent the leaders of the Republican Party from committing one of the worst political blunders in the history of our state. The Initiative was so poorly written that it would be better to withdraw the Initiative and submit a better written Initiative next year than to make this huge investment on passing an Initiative that has several major Red Flags. The last thing we need is yet another conservative Initiative overturned by the Supreme Court. This is especially true because conservatives have a long history of shooting themselves in the foot by promoting and passing poorly written Initiatives which are then overturned by the Supreme Court. This is my seventh article explaining the failure of conservative Initiatives to be properly written. It is time to do a better job of writing Initiatives.

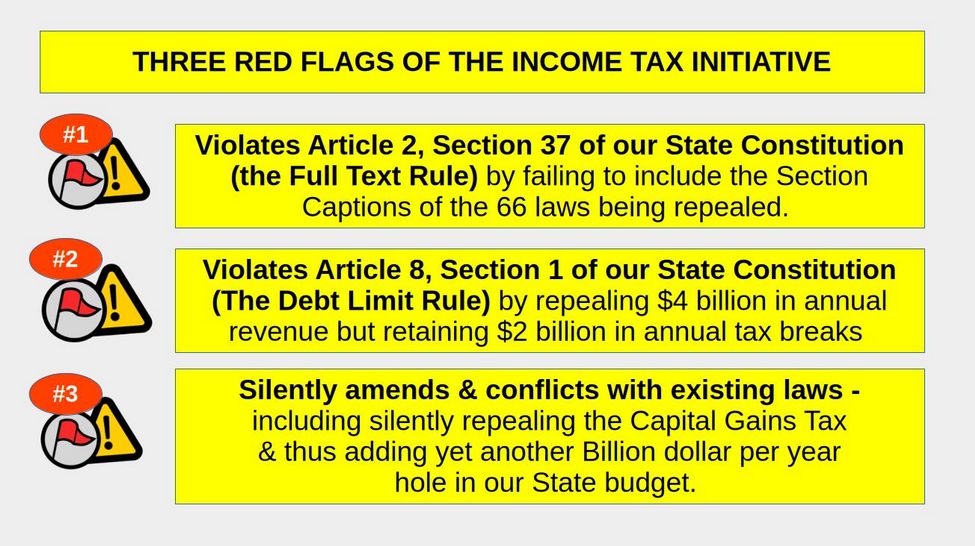

Three Red Flags with the Income Tax Initiative

In my prior article, I reviewed 3 “red flags” with the Income Tax Initiative.

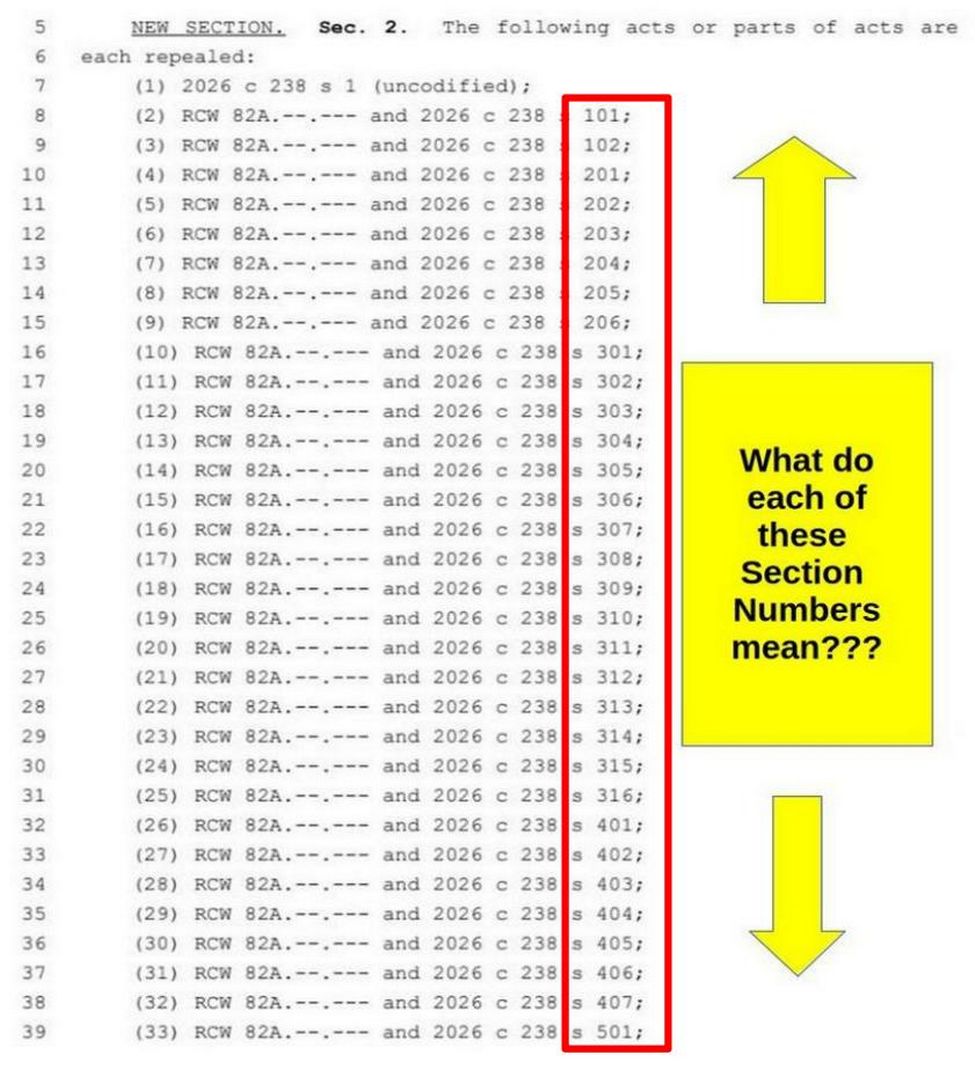

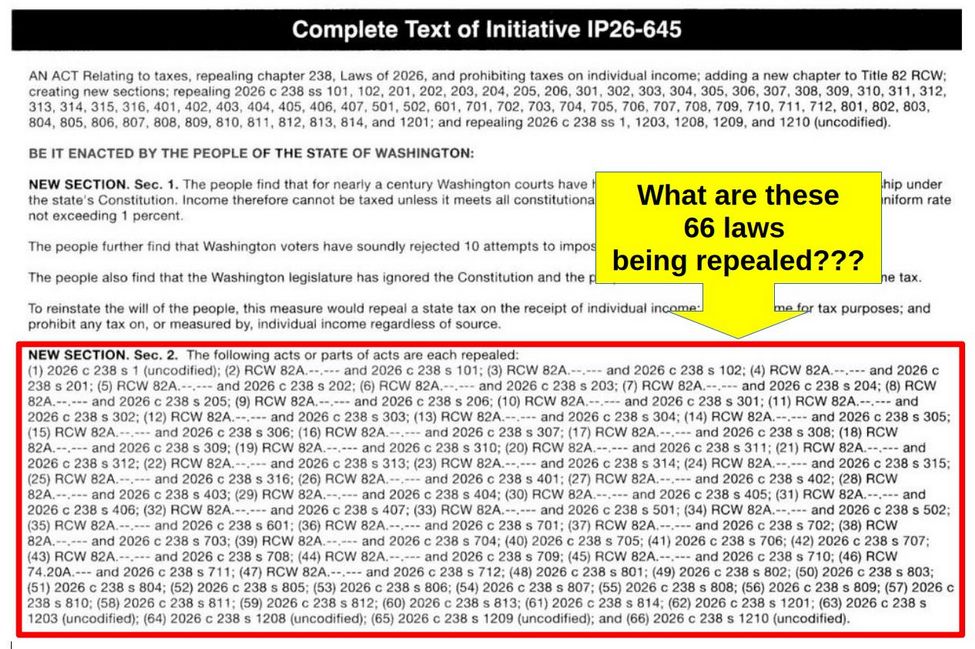

The first red flag is that the Initiative repeals 66 sections of Senate Bill 6346 by listing the 66 section numbers. But it fails to include the section “captions” for the 66 sections being repealed. The Section Captions are plain English labels describing the topic of the law or section of the law. Without these section labels, there is no way for voters to have even a clue as to what the 66 sections being repealed are even about. Two of the four pages of the Initiative are basically just a series of Section numbers. Below is an image of Page 2:

Had the Initiative included the captions for each section, voters would at least know what the section being repealed was about. For example, here are the initial sections of Senate Bill 6346 without their labels: Sec 101, Sec. 102, Sec. 201, Sec. 202, Sec. 203, Sec. 204, Sec. 205, Sec. 206. What are each of these sections being repealed about?

Here are these same sections with their section labels:

Sec. 101. DEFINITIONS.

Sec. 102. UNDEFINED TERMS—CONFORMITY WITH FEDERAL INTERNAL REVENUE CODE

Sec. 201. TAX IMPOSED—RATES.

Sec. 202. DISTRIBUTION OF TAX REVENUES.

Sec. 203. CREDIT FOR INCOME TAXES DUE TO ANOTHER JURISDICTION.

Sec. 204. CREDIT FOR BUSINESS AND OCCUPATION AND PUBLIC UTILITY TAXES.

Sec. 205. CREDIT FOR WASHINGTON CAPITAL GAINS TAXES.

By including the Section Captions, if a voter wanted to know what credit there would be for capital gains, they could read section 205 or the original bill. Here is a screenshot of the Repeal Section on the back of the printed Initiative Petitions which only show 66 numbers without Section Captions:

Clearly anyone signing this petition has no way of knowing what is in any of the sections being repealed. The intent of Article 2, Section 37 is that voters must be informed about what they are voting on and what the Initiative is repealing. This principle is so important that every bill considered by the legislature that repeals any law or section of law is required to include the section caption of the law or section of law being repealed.

At the end of this article, I provide a dozen examples of bills in the 2026 legislative session that had repeal sections. They all include the section captions. The importance of the Section Caption is further emphasized in the Code Reviser Bill Drafting Guide. Here is the example of a repeal section with a section caption on page 3:

NEW SECTION. Sec. 3. RCW 36.33.220 (County road property tax revenues, expenditure for services authorized) and 2001 c 212 s 25, 1973 1st ex.s. c 195 s 142, 1973 1st ex.s. c 195 s 32, & 1971 ex.s. c 25 s1 are each repealed.

Here is Rule 10b with another example of repeal section captions on page 12: Repealing sections of RCW. Cite the RCW section to be repealed, the section caption, and its session law history, from most current to original (see RCW 1.08.050). For example:

NEW SECTION. Sec. 1. RCW 43.88.120 (Revenue estimates) and 2000 2nd sp.s. c 4 s 13, 1991 c 358 s 3, 1987 c 502 s6, 1984 c 138 s 10, 1981 c 270 s 8, 1973 1st ex.s. c 100 s 7, & 1965 c 8 s 43.88.120 are each repealed.

Here is Rule 10c with another example of repeal section captions on page 12: Repealing more than one section of the RCW. Use subsection groupings, cite each RCW section to be repealed, the section caption, and its session law history, from most current to original. For example:

NEW SECTION. Sec. 1. The following acts or parts of acts are each repealed:

(1) RCW 70A.210.040 (Actions by municipalities validated) and 1975 c 6 s 4;

(2) RCW 70A.210.050 (Municipalities—Revenue bonds for pollution control facilities—Authorized—Construction—Sale, conditions—Form, terms) and 1983 c 167 s 174, 1975 c 6s 3, & 1973 c 132 s 5;

(3) RCW 70A.210.060 (Proceeds of bonds are separate trust funds—Municipal treasurer, compensation) and 1975 c 6 s 2; and

(4) 2002 c 301 s 1 (uncodified).

It would have only taken a little work to add these section captions to the Income Tax Initiative because the section captions were already listed in Senate Bill 6346. So why weren’t the Section Captions listed in the Income Tax Initiative?

Excuse #1 Misunderstanding RCW 1.08.017

Some have claimed that the Section Captions do not have to be listed. They point to RCW 1.08.017 which states that Section captions shall not be considered any part of the law: “Section captions... appearing in legislative bills shall not be considered any part of the law, and the reviser may omit such provisions from the Revised Code of Washington and annotations unless, in a particular instance, it may be necessary to retain such to preserve the full intent of the law.”

However, if you read the above RCW carefully, you will see that it is merely saying that the Section captions do not need to appear in the RCW version of the law. It does not say that Section captions do not need to appear in the bill (or Initiative) that creates the law. The legislature considers more than one hundred bills a year that have Repeal sections. If these repeal sections only listed the RCW number and not the caption describing what was in that RCW, legislators would be left clueless as to what the RCW being repealed was about. This is why Code Reviser is REQUIRED to include the Section captions for all laws being repealed by the legislature.

Excuse #2: It is up to the Code Reviser to include Section captions

The problem with this assumption is that the Code Reviser review process for an Initiative is radically different from Code Reviser Drafting process for a bill submitted to the legislature. For the hundreds of bills submitted to the legislature each year, the Code Reviser is responsible for writing the actual bill to be in keeping with their Bill Drafting Guide and to insure that every one of these bills also does not have any conflicts with any other state laws or with federal laws or with the State or Federal Constitution.

By contrast, Initiatives, which are required to be submitted to the Code Reviser for review, are NOT written by the Code Reviser. Instead, Initiatives are written by the Initiative sponsor and are only reviewed for formatting by the Code Reviser. Technically, the Code Reviser should point out obvious constitutional errors. But under RCW 1.08.028, the code reviser is not required to furnish a written opinion as to the constitutionality of any proposed Initiative.

The Washington Supreme Court has repeatedly ruled that Initiatives approved by the voters must meet the same Constitutional standards as bills approved by the legislature. So while Initiatives are subject to the same constitutional restrictions as bills from the legislature, the drafting and review process for an Initiative is radically different from the drafting and review process for a legislative bill. It is up to the sponsor of the Initiative to make sure the Initiative is written according to the rules in the Bill Drafting Guide. It is not up to the Code Reviser. This is why the Supreme Court is much more likely to reject an Initiative than to reject a bill by the legislature.

But that does not mean it is hard to write a valid Initiative to repeal a bill. This is because the Code Reviser did write Senate Bill 6346 and therefore there are Section Captions for every section in Senate Bill 6346.

By using the exact same language as the Code Reviser used in drafting the original bill, an Initiative Sponsor can be much more likely to wind up with a Constitutionally valid Initiative.

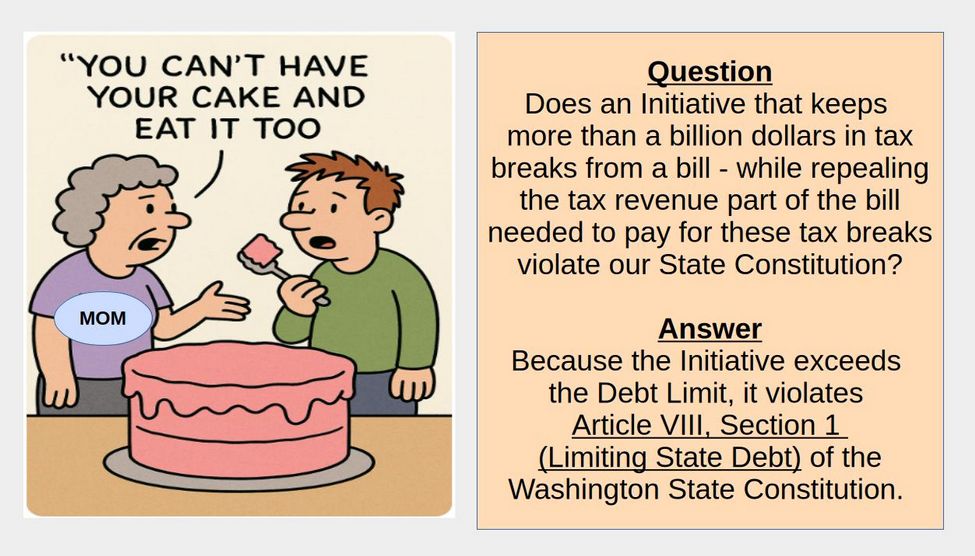

The Second Red Flag: Repealing several sections of Senate Bill 6346 while silently retaining several other sections of the same bill would put a $2 billion hole in our state budget – and therefore violate Article VIII, Section 1 (State Debt Limit) of the Washington State Constitution

To add insult to injury, not only does the Income Tax Initiative leave the voters in the dark about the 66 laws being repealed (due to the omission of section captions), it also leaves the voters in the dark about the 27 sections of Senate Bill 6346 that the Initiative leaves in place – because it does not even mention retaining them in the Initiative!

Here are the 27 Sections of Senate Bill 6346 that the Income Tax Initiative left in place: Sections 901, 902, 903, 904, 905, 906, 907, 908, 909, 910, 911, 912, 1001, 1002, 1003, 1101. 1102, 1103, 1104, 1105, 1106, 1107, 1202, 1204, 1205, 1206 and 1207. The only way to determine that these 27 sections were retained is to carefully read the entire 109 pages of Senate Bill 6346 while at the same time crossing off all of the numbers of the repealed sections listed in the Income Tax Initiative. Whatever is left over are the retained sections.

We need to carefully read all of these retained sections. It is only by carefully reading each of the above sections in the original bill and comparing each section to the Initiative that a voter might learn that the Initiative would repeal the $4 billion per year in Income Tax provisions in Part 2 but retain the $2 billion per year in Tax relief provisions in Parts 9, 10 and 11. The tax relief provisions are the expansion of the Working Families Tax Credit, the expansion of the Small Business Tax Exemption and a several hundred million dollar increase in Child Care subsidies.

Why did the Initiative Sponsors retain 27 sections of Senate Bill 6346?

Perhaps the sponsors of the Initiative may have been worried that if they repealed the $2 billion in “goodies”, that some voters might vote against the Initiative in order to retain the $2 billion in “goodies.” However, Section 1 Intent Item #11, at the bottom of Page 3 and top of Page 4 in Senate Bill 6346, states in part: “The legislature further intends that the tax imposed under this act operate together with certain tax reductions and tax credits enacted by this act as an integrated reform of the state tax code, and that repeal or invalidation of section 201 of this act would reinstate certain sales and use tax on items made exempt by this act and repeal working families tax credits and small business tax credits enacted by this act.”

The Initiative repeals Section 1 above and repeals the Income Tax in section 201 - but does not repeal the billions of dollars in Tax Relief offered in Section 9, 10 and 11. Thus, if the Initiative were approved by the voters, it would lead to a hole of at least $2 billion in the state budget.

While retaining these tax breaks is not actually mentioned in the Initiative, these goodies are a key feature of the Initiative being promoted by the sponsors. Here is the description of the Initiative copied from the Lets Go Washington website (unfunded goodies are underlined by me):

“What Does it do?”

“IP26-645 Repeals Bob Ferguson’s unconstitutional 9.9% tax on annual individual income over $1,000,000; prohibits taxes measured by individual income and taxes on individual income or the receipt of individual income; and defines “income.”

“Protects businesses, individuals, entrepreneurs and families in the state who shouldn’t be unfairly taxed.”

“Requires Olympia to fund the expansion of the Working Families Tax Credit, preserving tax relief for eligible low- and moderate-income working families.”

“Protects future exemptions for household necessities such as grooming and hygiene products, diapers, and over-the-counter drugs.”

“Provides small-business B&O relief, including the increased small-business tax credit and higher filing-relief threshold.”

“Leaves in place the bill’s future rollback of sales tax on certain services, including provisions tied to retail-sale definitions and technical corrections for services newly subject to sales tax.”

Constitutional Problems with the Income Tax Initiative

Even if the Supreme Court was willing to ignore the fact that the Section Captions for repealed Sections were not included in the Initiative, the Supreme Court will not be able to ignore this problem of creating a $2 billion hole in the state budget because cutting billions in state revenue while keeping billions in tax breaks and other goodies clearly violates

Article VIII, Section 1 of the Washington State Constitution which limits general obligation debt by capping annual debt to 9% of the average of general state revenues over the preceding 3 years. Here is a quote from Article VIII, Section 1:

“The aggregate debt contracted by the state shall not exceed that amount for which payments of principal and interest in any fiscal year would require the state to expend more than nine percent of the arithmetic mean of its general state revenues for the three immediately preceding fiscal years.”

Calculating the current Washington State Constitution Debt Limit

According to the Washington State Department of Revenue, general fund revenues totaled about $31 billion in 2023, $34 billion in 2024 and $36 billion in 2025. The average is about $34 billion per year. The nine percent Debt Limit on $34 billion in revenue is about $3 billion debt limit. But this is the total debt allowed. By state law (RCW 39.42.140), the State Finance Committee enforces a lower "working debt limit" (currently 7.75%) to reserve emergency capacity and handle economic uncertainties. In plain English, Washington state debt is already at almost 8% of $34 Billion or about $2.7 billion a year. Therefore, any bill or initiative that calls for spending more than $300 million in tax breaks and other goodies without providing a revenue source to pay for the tax breaks violates Article VIII, Section 1 (Limiting State Debt) of the Washington State Constitution.

Imagine if the legislature passed this Initiative, as written, without providing a funding source for the $2 billion in goodies. They would clearly be violating Article VIII, Section 1. Just as the legislature is required to comply with the State Debt Limit, so are drafters of Initiatives.

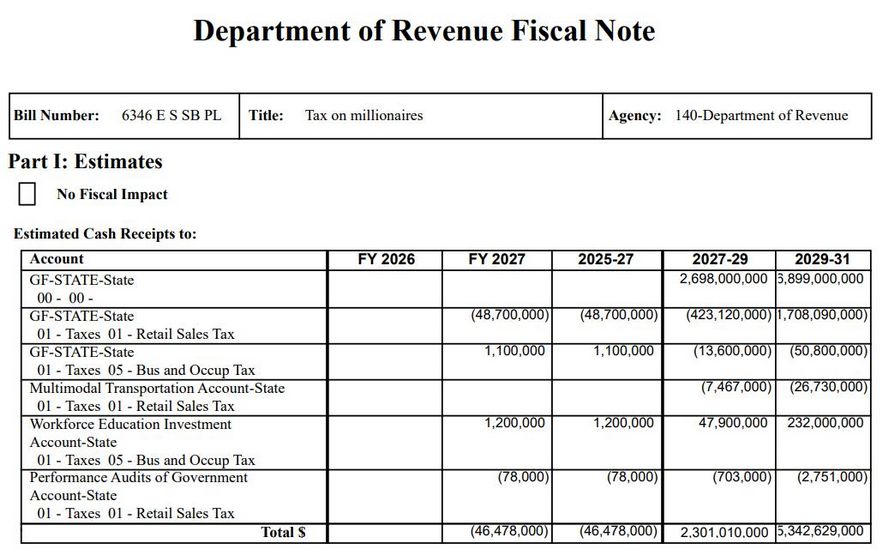

What are the exact estimates of the increase in State Revenue in Senate Bill 6346 and the cost of all of the goodies promised by both Senate Bill 6346 and the Income Tax Initiative?

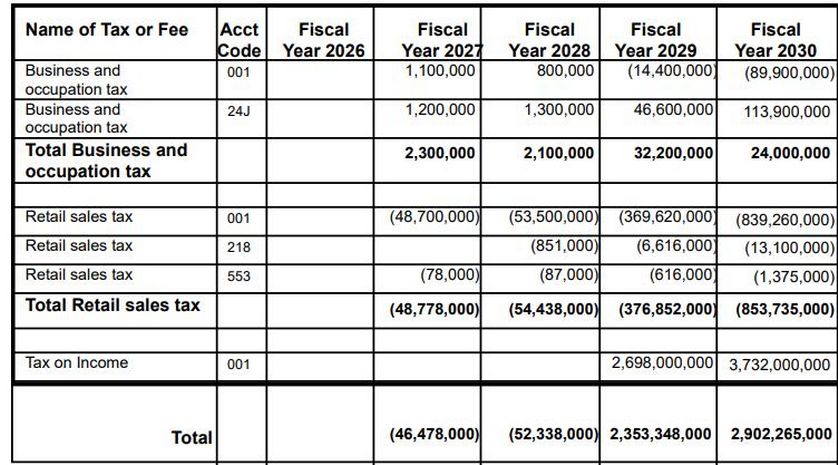

Until now, we have been using an estimate of $4 billion a year in revenue from the Millionaires Income Tax and $2 billion a year in goodies promised by both Senate Bill 6346 and the Income Tax Initiative. But the actual numbers are in the Fiscal Note to Senate Bill 6346 which you can download from this link. The Fiscal Note is 149 pages long. On page 37 is an estimate per biennium or two year period of time. Income Tax Revenue is estimated to be $7 billion per biennium. The sales tax breaks are estimated to be $1.7 billion per biennium. The Business and Occupation tax is $50 million per biennium. The work force tax credit program is $232 million per biennium. After deducting these goodies, the net income from Senate Bill 6346 would be $5.342 billion per the 2029 to 2031 biennium.

The problem with the above chart is that the entire program does not phase in until 2030. So a better estimate of both the revenue and the cost of the goodies is provided in the following annual chart which is on page 116 and looking at the year 2030.

Here we see that in 2030, the total revenue from the millionaires income tax in 2030 would be $3.732 billion per year in today’s dollars. With 4 years of inflation, this will be about $4 billion in 2030 dollars.

Of this $4 billion, but not shown on the above chart (but is shown on the previous chart), about $232 million is assigned to be spent on the annual cost of the work force tax credit program. The goody expands the Working Families Tax Credit from the current 350,000 families to about 800,000 families, providing direct financial relief that helps low income families raising children. The credit is about $660 to $1,000 per family per year.

The Business and Occupation Tax break is about $90 million a year and the retail sales tax break is about $853 million per year. In addition, the Income tax revenue will be used to expand state funded day care subsidies for poor families. Currently, the state spends about $600 million per year on day care subsidies. On page 116, the Fiscal Note explains that the Income Tax bill would add about another $160 million per year to this program.

There are a few other tax breaks in Senate Bill 6346 that are also retained by the Income Tax Initiative. But to keep this simple, we will skip these. Thus, the total amount of goodies per year is about 232 plus 90 plus 853 plus 160 equals 1,335 million or 1.335 billion dollars. With inflation, the actual total amount of the goodies by 2030 will be about 1.5 billion dollars.

So a more accurate statement is that the Initiative would repeal $4 bullion in revenue but keep $1.5 billion in tax breaks and other goodies. Imagine the legislature passing a bill with $1.5 billion in new spending – but not providing any funding source to pay for the new spending. The legislature could not pass such a bill because it would violate the Article VIII, Section 1 Debt Limit. The same is true for an Initiative. It is a violation of Article VIII, Section 1 for the Initiative to keep $1.5 billion in spending but not provide any revenue to pay for it. It is essentially lying to the voters by telling them they will all get a free pony – when in fact none of them will get a free pony.

The Initiative is not a complete act

It is also likely that the Court would toss the entire Initiative over this problem simply because, while Senate Bill 6346 was a “complete act” – carefully drafted by the Code Reviser to make sure their were no conflicts with existing laws – the Initiative is NOT A COMPLETE ACT, because it amends (repeals) some parts of Senate Bill 6346 while retaining other parts of Senate Bill 6346. The Supreme Court has repeatedly stated that they will look much more closely at Initiatives which are not a complete Act than they will look at Initiatives which are a complete act.

The way to avoid this problem, as I stated in my prior article, was to repeal the entire Senate Bill 6346 – repeal both the $4 billion in new taxes and the $2 billion in goodies. Since Senate Bill 6346 was a complete act, the repeal of the entire thing would also be a complete act and the Supreme Court would not have to worry so much about conflicts with other laws because they would know that the Code Reviser had already researched and resolved this issue.

The Supreme Court would also not have to worry about being blamed for putting a one to two billion dollar hole in the State budget. Retaining 27 sections of Senate Bill 6346 may get the sponsors of the bill a few more votes. But it also greatly increases the odds that the Supreme Court will reject the Initiative. So the safe thing to do is to write only Initiatives that are COMPLETE ACTS.

The third Red Flag: Silently repealing the Capital Gains Tax

In addition, the Initiative appears to silently repeal the Capital Gains tax. Look carefully at the New Section 1 which states in part: “This measure would… prohibit any tax on, or measured by, individual income regardless of source.”

Then look carefully at the “Definition of Income” in the New Section 3 on page 3 of the Initiative: “Income” means any gain or benefit measured in money derived from an individual’s capital, labor, property or other source.”

A plain English reading of the above two sentences would include the idea that a gain based on capital (AKA a capital gain) would be income and therefore would be prohibited from being taxed – despite the fact that the Capital Gains tax was affirmed by the voters just a couple of years ago.

Not only is this a silent amendment, but since the Capital Gains tax brings in about a billion dollars a year in state revenue, repealing the Capital Gains tax would add another billion dollar hole in the state budget – making the total state budget hole created by the Initiative to be about $2.5 to $3 billion dollars – another violation of Article 8, Section 1 of our Constitution.

This is the sort of legal conflict with existing laws that the Code Reviser would warn a legislator about if they attempted to include such a definition in a bill. The best way to avoid conflicts with existing laws is to NOT include any new text when trying to delete a bill. Just delete the entire bill. No additions or subtractions without a very careful review of all possible conflicting laws.

Example: The Free Pony Initiative

Cutting $4 to $5 billion in state revenue while retaining $2 billion in tax breaks and other goodies is like claiming that every child will get a free pony if their parents vote for the Initiative.

Imagine that the legislature passed Senate Bill 9999 that included both a Millionaires Income Tax with $4 billion in new revenue and a Capital Gains Tax with $1 billion in new revenue for a total of $5 billion in new revenue. To entice the voters into supporting Senate Bill 9999, the bill also included a $1,000 pony for all one million families with kids in the public schools - AND a $2,000 annual check for each of these one million families. The total cost of these goodies would be about $2 to $3 billion per year.

Next imagine that conservatives wrote an Initiative to repeal the Millionaires Income Tax - and included a definition of Income that silently repealed the Capital Gains Tax – but their Initiative kept the parts of Senate Bill 9999 that gave every family with a child in the public schools a $1,000 pony and an annual check for $2,000.

Now imagine that the Washington Supreme Court decided that omitting the Section Titles was not a major violation of Article 2, Section 37 (the Full Text Rule) and that putting a $3 billion dollar hole in the State budget was not a major violation of Article 8, Section 1 (the State Debt Limit) and that the Definitions section of the Initiative did not silently amend the Capital Gains Tax law. Instead, the Supreme Court decided to honor the “will of the voters” rather than the plain meaning of our State Constitution.

Think about the massive problem passing such a fiscally irresponsible Initiative would create. Where would the legislature come up with the money to give each child a free pony? Where would the legislature come up with the money to give one million families an annual check for $2,000?

The only good news in this example is that the judges on the Supreme Court swear an Oath to uphold the Washington State Constitution – regardless of the popularity of any Initiative that violates our Constitution.

So our legislature will not likely have to deal with such a problem. But what about all of the voters who voted for the Initiative under the promise that they would get a free pony and an annual check for $2,000? They will blame and be angry at the Initiative sponsors who tricked them.

The fourth and final Red Flag: There has never been an Initiative or legislative bill written as badly as the 2026 Income Tax Initiative

One person who read my prior article claimed that he ran my concerns past some attorneys and they claimed that the Income Tax Initiative was validly written despite the lack of section captions and despite the failure to mention the sections of the bill not repealed and despite the failure to comply with the Constitutional State Debt Limit and despite the addition of a definitions section that clearly conflicts with and silently amends a recently passed law such as the Capital Gains tax.

My reply was to challenge his attorney friends to provide at least ONE EXAMPLE of an Initiative or a legislative bill with a Repeal Section that did not include Section Captions. Neither this person nor any of his attorney friends have been able to provide such an example.

I knew this would be the case because I had already researched all of the Initiatives passed and not passed during the last 20 years that had a Repeal Section. I already knew that there were no Initiatives with a Repeal section that did not include the Section Caption.

Not only has there never been a Repeal Initiative without a Section Caption, there has never been an Initiative that repealed 66 sections of a bill while retaining 27 sections. There has also never been an Initiative that repealed $4 billion in new taxes while retaining $2 billion in new goodies.

So should this bill pass the voters, the Supreme Court will be confronted with a question more complex than any question it has ever faced. Do they reject a badly written but popular Initiative? Or do they put a 2 to 3 billion dollar hole in the state budget?

Do they acknowledge that there is no way that the voters knew what was in all of the 66 Sections that were repealed – and certainly the voters would have no way to know what was in the 27 sections that were retained.

Or do they break new ground and let the Initiative stand despite the fact that none of the voters had any way of knowing what the Initiative actually does and does not do? Do you really think that the Supreme Court will let such a fatally flawed Initiative stand???

But the real question is why put the Supreme Court in such a difficult NO WIN situation in the first place?

Wouldn’t it be far better to pull the poorly written Income Tax Initiative now – and then come back in the Spring with a properly written Income Tax Initiative that does not suffer from all of these Red Flags?

Real leadership is having the courage and wisdom to listen to dissent and admit when you make a mistake. Real leadership is being able to change directions when the path you are currently on will only wind up wasting tens of thousands of hours of volunteer time and millions of dollars in volunteer donations. It is not my intention to “attack the drafters of the Initiative.” Just the opposite. I wrote the prior article and this article to convince them to change course before it is too late.

But should they not change course – and should the Supreme Court rule against them in a year or two from now – at least I will be able to say that I tried to prevent this disaster. And maybe then they will learn to do a more careful job of writing a valid Initiative by following the rules in the Code Reviser Bill Drafting Guide and by following all relevant provisions of the Washington State Constitution.

What Real Tax Reform would look like

The drafters of the Income Tax Senate Bill 6346 and the drafters of the Income Tax Initiative both claim they are in favor of “tax reform.” But neither Senate Bill 6346 or the Income Tax Initiative actually provides any significant tax reform.

As I explained in my prior article, the real problem with our state taxes is that the new budget calls for $40 billion in state spending – which is more than double the size of state spending just 14 years ago – even when accounting for Inflation and population growth.

Real tax reform would cut state taxes in half by cutting the size of state government in half. Instead of a state budget that raises and spends $40 billion a year, we need to elect people who will pledge to limit state spending and state taxes to under $20 billion a year.

I provided several ideas for how to do this in my last article, so I will not repeat them here. But we could easily save a billion dollars a year in child care subsidies – and at the same time cut child care costs in half (from $2,000 per month per child back to $1,000 per month per child) simply by ending the over-regulation of childcare – over-regulation which put tens of thousands of local neighborhood childcare providers out of business. This would also create tens of thousands of new jobs.

We could also reduce state spending by reducing the over-regulation of public schools. Article 2, Section 28 of our state constitution states that “The legislature shall pass no special laws… regarding the management of our public schools.” Despite this fact, the legislature has passed 484 laws regarding the management of our public schools. Each one of these laws requires an administrator at OSPI to harass the schools into compliance – and another paper pusher at every school district in the state to file Compliance Reports to OSPI. Many of these paper pushers are paid more than the President of the United States.

Imagine returning to local control of public schools and rolling all of these 484 regulations in half – back to 242 school regulations – so that local schools could hire more teachers instead of more administrators. Instead of having 800 employees and consultants at OSPI, we could cut OSPI in half and go back to the days of Randy Dorn when OSPI only had 400 employees – and Washington state was 5th in the nation in student scores on the 8th grade math test.

The Constitution prohibits an Initiative (or the legislature) from tying the hands of a future legislature. So the only way we will ever slow down the skyrocketing State spending is by electing legislators who will take real tax reform more seriously.

Questions and Answers

Email me any questions you may have about the problems with the Income Tax Initiative and I will do my best to answer them. Here are some questions submitted by readers:

Question 1: Why don't you lend your support in writing initiatives that will survive scrutiny by the WA supreme court?

I have offered to help. I began writing articles on how to write a constitutionally valid Initiative more than a year ago. Today’s article was the seventh article I have written on this subject in the past 12 months. In each of these articles, I have explained precisely how to correct the defects of their past and current Initiatives. In the case of the Income Tax Initiative, all that is needed is to write the section numbers and captions being repealed. Nothing more or less. Sadly, the Petition sponsors are not interested in a simple repeal of Senate Bill 6346. But the way they want to do it does not comply with our state constitution.

As for signers not reading the actual petition, you are right. Signers rarely read the petitions they sign. They simply trust that the Initiative sponsors did a good job writing the Initiative and are telling them the truth about the Initiative. But the Supreme Court will read the petition and thus the Initiative must comply with our State Constitution – which is actually not that hard to do.

Question 2: If an Initiative complied with Article 2, Section 37 of the Washington state constitution, wouldn’t it take up too much space and not fit on the back of the Initiative Petition sheets?

The Income Tax Initiative, as submitted to the Secretary of State is 4 pages long. If it were properly written, with section titles repealing all 93 sections of Senate Bill 6346, but with no additional text, it would have been 6 pages long. This would have easily fit on a petition sheet without any change in the font size. In fact, there have been 8 Petitions approved by the voters since 2008 that were 10 or more pages long. The average page length of these 8 successful Initiatives was 20 pages. Here is a table of these Initiatives:

Question 3: Why can't we force the supreme court to approve an initiative as being constitutional before it is presented to the people for signatures and wastes a lot of people's time and effort?

The answer is that the Supreme Court decided more than 100 years ago that Initiatives must follow the same rules as bills from the legislature. The legislature proposes hundreds of laws every year. The Court will only review the bills that have become actual law and even then only if someone files a complaint. Same is true of Initiatives. They must first be approved by the voters in an election and then be challenged in Court before the Court will issue an opinion. It is therefore up to the Initiative sponsors to be very careful in writing Initiatives. But the good news is that it is pretty easy to predict how the court will rule simply by reading their many previous rulings during the past 100 years – and by reading the Code Revisers Bill Drafting Guide. This is why in all seven of my past articles on writing Initiatives, I included many quotes from the Supreme Court and also quotes from the Bill Drafting Guide.

The real problem has been and continues to be people writing Initiatives without reading the many past Supreme Court opinions – and people ignoring the Code Revisers Bill Drafting Guide. I think this problem will only be corrected when people like you demand that Initiative sponsors do a more carefully job of writing Initiatives so that they comply with our state constitution.

Question 4: If the voters pass this Income Tax Initiative this November and it is challenged in court, how long will it take before the Washington Supreme Court makes a ruling to overturn it?

If the Income Tax Initiative is approved by the voters this November, it is certain that it will be challenged in court within weeks. It will then follow a path similar to the Natural Gas Initiative 2066 which was approved by the voters in November 2024 and then challenged in King County Superior Court. In March 2025, a King County judge issued a verbal ruling that Initiative 2066 violated Article 2, Section 37 of our State Constitution (among other defects) and blocked the Initiative from taking effect. In May 2025, this judge issued a written opinion with the same conclusion. This opinion was then immediately appealed by the Initiative sponsors to the Washington Supreme Court. It took 7 months to file all of the legal briefs. The Supreme Court heard oral arguments from both sides in January 2026 – but still has not issued a written opinion. It is highly likely that the Supreme Court will issue an opinion rejecting the natural gas initiative sometime in the next couple of months.

Assuming a similar timeline for the Income Tax Initiative, it will likely be ruled to be unconstitutional by a King County Judge in Spring 2027 and will be appealed by the Initiative sponsors to the Supreme Court shortly after a written opinion is published in May 2027. It will take about 7 months to file all of the legal briefs. The Supreme Court will hear oral arguments from both sides in January 2028 – but likely delay issuing a permanent ruling blocking the Income Tax Initiative until July 2028.

This timeline means that the only way we can get a validly written Income Tax Initiative on the 2028 general election ballot is if the sponsors of the current Initiative pull their Initiative and do not put it on the Fall 2026 ballot. If they instead continue down the path they are currently on, the net effect of their actions will be to insure that the Income Tax takes effect in 2028.

Conclusion

If you agree that it is time to start writing more valid Initiatives and time to promote real tax reform, then join our Washington Parents Network and start attending our monthly meetings which are held on the first Sunday of every month from 4 to 5 pm. Our June 2026 meeting will be on June 7th.

12 Examples of 2026 Bills with Repeal Sections and Section Captions

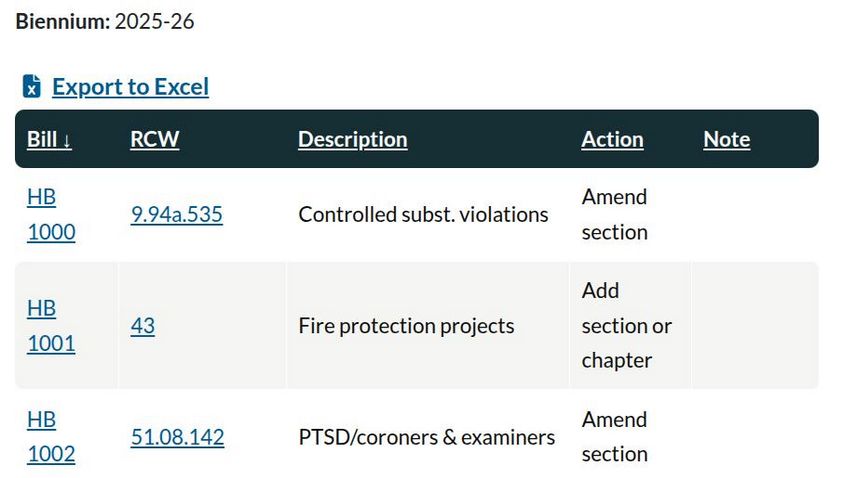

You can access an official chronological list of all bills enacted and chapters repealed during past legislative years using the state's Session Laws. Click View Complete Table. Here is what the table looks like:

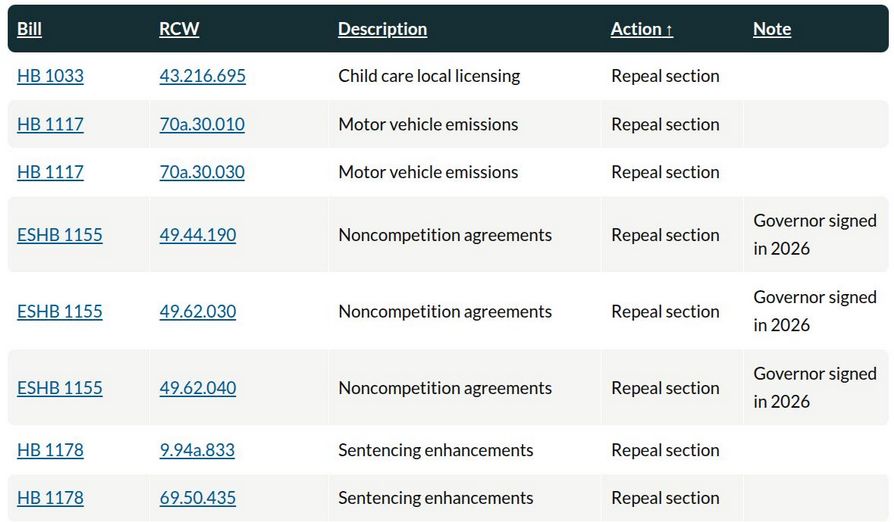

Then click on Action. Then click Action again. This will then show a list of all bills with Repeal Sections. Here is what the table looks like now:

Scroll down and you will see that there are more than 100 bills with repeal sections. All of these bills have section captions added to the repeal sections. Below are a dozen examples of these bills. (all section captions are in bold).

Example 1: House Bill 1033 page 9:

NEW SECTION. Sec. 4. RCW 43.216.695 (County regulation of family day-care centers—Twelve-month pilot projects) and 2005 c 509 s1 are each repealed, effective July 1, 2026.

Example 2: House Bill 1117 page 2

NEW SECTION. Sec. 2. The following acts or parts of acts are each repealed:

(1) RCW 70A.30.010 (Department of ecology to adopt rules to implement California motor vehicle emission standards) and 2020 c 143 s 1, 2020 c 20 s 1366, 2010 c 76 s 1, & 2005 c 295 s 2; and

(2) RCW 70A.30.030 (New vehicle greenhouse gas emissions disclosure—Rule-making authority) and 2020 c 143 s 2, 2014 c 76 s 8, & 2008 c 32 s 2.

Example 3: House Bill 1155 passed page 7

NEW SECTION. Sec. 8. The following acts or parts of acts are each repealed:

(1) RCW 49.62.030 (When void and unenforceable against independent contractors) and 2019 c 299 s 4;

(2) RCW 49.62.040 (Dollar amounts adjusted) and 2019 c 299 s 5; and

(3) RCW 49.44.190 (Noncompetition agreements for broadcasting industry employees—Restrictions—Trade secrets protected) and 2005 c176 s 1.

Example 4: House Bill 1178 page 46

NEW SECTION. Sec. 8. The following acts or parts of acts are each repealed:

(1) RCW 9.94A.833 (Special allegation—Involving minor in felony offense—Procedures) and 2008 c 276 s 302; and

(2) RCW 69.50.435 (Violations committed in or on certain public places or facilities—Additional penalty—Defenses—Construction— Definitions) and 2022 c 16 s 93, 2015 c 265 s 37, & 2003 c 53 s 346.

Example 5: House Bill 1237 page 5

NEW SECTION. Sec. 3. The following acts or parts of acts are each repealed:

(1) RCW 80.50.075 (Expedited processing of applications) and 2022 c 183 s 18, 2006 c 205 s 2, 1989 c 175 s 172, & 1977 ex.s. c 371 s17; and

(2) RCW 80.50.320 (Governor to evaluate council efficiency, make recommendations) and 2001 c 214 s 8

Example 6: House Bill 1262 page 14

NEW SECTION. Sec. 7. RCW 44.28.810 (Review of governor's inter-agency coordinating council on health disparities—Report to the legislature) and 2006 c 239 s 7 are each repealed

Example 7: House Bill 1295 passed page 9

NEW SECTION. Sec. 11. The following acts or parts of acts are each repealed:

(1) RCW 28A.410.285 (Teacher preparation programs) and 2019 c 295 s 203;

(2) RCW 28A.415.350 (Professional development learning opportunities—Partnerships) and 2009 c 539 s 4 & 2007 c 402 s 7;

(3) RCW 28A.415.360 (Learning improvement days—Eligibility— Reports) and 2019 c 252 s 117, 2009 c 548 s 403, & 2007 c 402 s 9; and

(4) RCW 28A.415.400 (Reading instruction and early literacy— Professional development) and 2013 2nd sp.s. c 18 s 103.

Example 8: House Bill 2251 passed page 47

NEW SECTION. Sec. 21. The following acts or parts of acts are each repealed:

(1) RCW 70A.65.250 (Climate investment account) and 2025 c 424 s973 & 2024 c 376 s 911;

(2) RCW 70A.65.260 (Climate commitment account) and 2025 c 424 s974, 2023 c 475 s 939, 2022 c 179 s 17, & 2021 c 316 s 29; and

(3) RCW 70A.65.270 (Natural climate solutions account) and 2021 c316 s 30.

Example 9: Senate Bill 5294 passed page 4

NEW SECTION. Sec. 2. The following acts or parts of acts are each repealed:

(1) RCW 18.08.240 (Architects' license account) and 2018 c 207 s9, 1991 sp.s. c 13 s 2, 1985 c 57 s 4, & 1959 c 323 s 15;

(2) RCW 18.39.810 (Funeral and cemetery account) and 2018 c 299 s5919 & 2009 c 102 s 24;

(3) RCW 18.96.210 (Landscape architects' license account) and 2009 c 370 s 17;

(4) RCW 18.140.260 (Real estate appraiser commission account) and 2005 c 339 s 20 & 2002 c 86 s 241;

(5) RCW 18.220.120 (Geologists' account) and 2000 c 253 s 13; and

(6) RCW 18.310.160 (Appraisal management company account) and 2010 c 179 s 16.

Example 10: Senate Bill 5520 passed page 11

NEW SECTION. Sec. 10. RCW 4.100.020 (Claim for compensation—Definitions) and 2013 c 175 s 2 are each repealed.

Example 11: Senate Bill 6022 page 36

NEW SECTION. Sec. 12. The following acts or parts of acts are each repealed:

(1) RCW 13.40.301 (Department to protect younger children in confinement from older youth confined pursuant to 2018 c 162) and2018 c 162 s 8;

(2) RCW 13.04.800 (Report to legislature—2021 c 206 ss 2 and 3; 2019 c 322 ss 2-6; 2018 c 162) and 2021 c 206 s 9, 2019 c 322 s 5, & 2018 c 162 s 9;

3) RCW 72.01.412 (Eligibility for community transition services) and 2023 c 470 s 3018, 2021 c 206 s 2, & 2019 c 322 s 6;

(4) RCW 43.216.180 (Education of students in the custody of juvenile rehabilitation facilities—Duties—Creation of a comprehensive plan) and 2019 c 322 s 7;

Example 12: House Bill 1995 This is an example of how to repeal more than 30 laws… Note that the Section captions for all 30 law are all included in this bill. This is what the Income Tax Initiative Repeal Sections should have looked like:

NEW SECTION. Sec. 1. The following acts or parts of acts are each repealed:

(1) RCW 82.16.046 (Exemptions—Operation of state route No. 16) and 1998 c 179 s 5;

(2) RCW 82.29A.132 (Exemptions—Operation of state route No. 16) and 1998 c 179 s 6;

(3) RCW 82.45.190 (Exemptions—State route No. 16 corridor transportation systems and facilities) and 1998 c 179 s 7;

(4) RCW 82.08.02566 (Exemptions—Sales of tangible personal property incorporated in prototype for parts, auxiliary equipment, and aircraft modification—Limitations on yearly exemption) and 2003 c168 s 208, 1997 c 302 s 1, & 1996 c 247 s 4;

(5) RCW 82.12.02566 (Exemptions—Use of tangible personal property incorporated in prototype for aircraft parts, auxiliary equipment, and aircraft modification—Limitations on yearly exemption) and 2003 c168 s 209, 1997 c 302 s 2, & 1996 c 247 s 5;

(6) RCW 82.08.02568 (Exemptions—Sales of carbon and similar substances that become an ingredient or component of anodes or cathodes used in producing aluminum for sale) and 1996 c 170 s 1;

(7) RCW 82.12.02568 (Exemptions—Use of carbon and similar substances that become an ingredient or component of anodes or cathodes used in producing aluminum for sale) and 1996 c 170 s 2;

(8) RCW 82.04.4482 (Credit—Sales of electricity or gas to an aluminum smelter) and 2004 c 24 s 9;18

(9) RCW 82.16.0498 (Credit—Sales of electricity or gas to an aluminum smelter) and 2004 c 24 s 13;20

(10) RCW 82.12.0265 (Exemptions—Use by bailee of tangible personal property consumed in research, development, etc., activities) and 1980 c 37 s 64;

(11) RCW 36.100.090 (Tax deferral—New public facilities) and 1995 1st sp.s. c 14 s 6;

(12) RCW 82.12.024 (Deferral of use tax on certain users of natural or manufactured gas) and 2001 c 214 s 10;

(13) RCW 82.04.545 (Exemptions—Sales of electricity or gas to silicon smelters) and 2017 3rd sp.s. c 37 s 705 & 2017 3rd sp.s. c 37s 704;

(14) RCW 82.16.315 (Exemptions—Sales of electricity or gas to silicon smelters) and 2017 3rd sp.s. c 37 s 703 & 2017 3rd sp.s. c 37 s 702;

(15) RCW 82.16.0495 (Credit—Electricity sold to a direct service industrial customer) and 2001 c 214 s 11;

(16) RCW 36.102.070 (Deferral of taxes—Application by public stadium authority—Department of revenue approval—Repayment— Schedules—Interest—Debt for taxes—Information not confidential) and 1997 c 220 s 201;

(17) RCW 82.08.02569 (Exemptions—Sales of tangible personal property related to a building or structure that is an integral part of a laser interferometer gravitational wave observatory) and 1996 c113 s 1;

(18) RCW 82.12.02569 (Exemptions—Use of tangible personal property related to a building or structure that is a part of a laser interferometer gravitational wave observatory) and 1996 c 113 s 2;

(19) RCW 82.04.421 (Exemptions—Out-of-state membership sales in discount programs) and 1997 c 408 s 1;

(20) RCW 82.04.4331 (Deductions—Insurance claims for state health care coverage) and 1988 c 107 s 33;

(21) RCW 82.04.4295 (Deductions—Manufacturing activities completed outside the United States) and 1980 c 37 s 15;

(22) RCW 82.04.447 (Credit—Natural gas purchased by direct service industrial customers—Reports) and 2001 c 214 s 9;

(23) RCW 84.36.047 (Nonprofit organization property used for transmission or reception of radio or television signals originally broadcast by governmental agencies) and 1984 c 220 s 4 & 1977 ex.s. c 348 s 1;

(24) RCW 82.04.367 (Exemptions—Nonprofit organizations that are guarantee agencies, issue debt, or provide guarantees for student loans) and 1998 c 324 s 1 & 1987 c 433 s 1;

(25) RCW 82.23B.030 (Exemption) and 2015 c 274 s 15, 1992 c 73 s 9, & 1991 c 200 s 803;

(26) RCW 82.08.965 (Exemptions—Semiconductor materials manufacturing) and 2024 c 261 s 5;

(27) RCW 82.12.965 (Exemptions—Semiconductor materials manufacturing) and 2024 c 261 s 7;

(28) RCW 82.08.970 (Exemptions—Gases and chemicals used to manufacture semiconductor materials) and 2024 c 261 s 6;

(29) RCW 82.12.970 (Exemptions—Gases and chemicals used to manufacture semiconductor materials) and 2024 c 261 s 8;

(30) RCW 82.04.448 (Credit—Manufacturing semiconductor materials) and 2024 c 261 s 4;

(31) RCW 82.04.426 (Exemptions—Semiconductor microchips) and 2024 c 261 s 3;

(32) RCW 82.04.4332 (Deductions—Tuition fees of foreign degree granting institutions) and 1993 c 181 s 10;